Latest news about Bitcoin and all cryptocurrencies. Your daily crypto news habit.

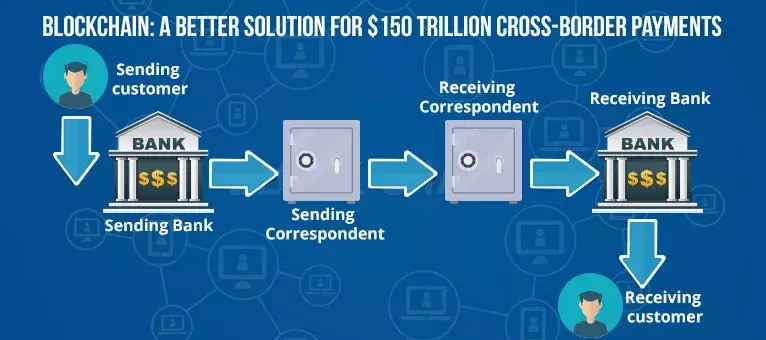

Did you know that cross-border payments were more than $150 trillion in 2015? Major users of these payments were individuals. But businesses transacted more of this $150 trillion. $200 billion revenue was generated by the payments industry through the services they provided to payers and payees. It is to be noted that about 80% of this business was from B2B. So this is the magnitude in which the cross border payments are being carried out. I'll cover how Blockchain is a promising alternative to the current correspondent banking system shortly. By the way Intellipaat is offering robust hands-on training in Blockchain. You might want to check it out.

Inconvenience due to current correspondent banking

You are now familiar with the volume of correspondent banking transactions. Let's see what problems it faces currently:

Huge time required - McKinsey research and analysis report on cross border payments was produced in 2015. It says that 3 to 5 days is the average time required to complete a cross border payment. This includes the final transfer through domestic payment network.

Opacity - Imagine you have sent $5000 to your relative in Australia. Most probably you and your recipient relative will be restless as to when will the money get transferred, how much will get deducted and how much will finally reach the intended destination which the relative can take. This is the case with those people who have geographic distance between them and their relatives and who frequently make payments to them. The problem is much worse when one has to quickly trace transactions as in the case when incorrect account numbers were provided while transferring the money.

Cost - Fees keeps on accumulating after every step in the money transfer. Money has to traverse from sender's bank to the national correspondent bank or it has to traverse from one correspondent bank to another. Add foreign exchange fee to that and the cost involved becomes a burden. For very high amount of money to be transferred the charges for correspondent banking is around 2 - 3%. For smaller denominations the charges can go upto 10% also. Sometimes the cost will be put on the recipient also.

To trump over these inefficiencies Blockchain technology can be. As the global network of correspondent banking is decentralized it shouldn't come as a surprise that innovation in that space also comes through decentralized network solutions. Blockchain could well be the backbone of the correspondent banking transactions as it certainly has the potential. Blockchain doesn't move digital assets physically but they make such changes in asset ownership that it just can't be tampered with. This is the main reason why it is projected to replace the current correspondent banking. Eager local exchanges will be on heels in providing real-time liquidity for these blockchain transactions in local currency obviously in return for ownership of assets.

How and who uses Blockchain technology in correspondent banking?

Interbank Information Network (IIN) was formed when J.P. Morgan joined hands with Royal Bank of Canada and Australia and New Zealand Banking Group Limited. IIN was incepted to lubricate the global payment process so that with just few steps and enhanced security, payments could reach beneficiaries. This Blockchain technology is still very young and is yet to gain global reach and acceptance. But these are global players in banking and they have recognized the importance and potential of Blockchain technology.

Remember I said earlier that correspondent banking transactions take about 3 to 5 days. Blockchain powered IIN is all set to improve customer experience (CX) as the time taken for correspondent banking transactions which is in days will essentially be reduced to hours. There are huge costs associated with payment delays as said earlier but IIN is set to resolve this issue. There are multiple layers of communication to verify and process transactions between payment participants. Blockchain backed IIN will greatly lower the participants needed to respond to the compliance and the rest of data related queries that are mainly responsible for delaying payments. QuorumTM is a variant of Ethereum Blockchain and is responsible for powering IIN. This system focuses heavily on providing privacy and therefore secure data sharing through IIN is very much possible.

Conclusion

Correspondent banking is only one of applications of Blockchain. Smart contracts, voting, detecting counterfeit drugs, supply chain auditing, land deals all find good applications in Blockchain. You might obviously be familiar with bitcoin. Well, Blockchain is the medium through which it gets traded. Did you know that Australia is planning to use Blockchain in its stock market? That's how much potential this wonderful technology has. Blockchain may essentially become synonymous with the future of trusted transactions judging by its growth trajectory.

Author Bio:

Vaishnavi Agrawal loves pursuing excellence through writing and have a passion for technology. She has successfully managed and run personal technology magazines and websites. She currently writes for intellipaat.com, a global training company that provides e-learning and professional certification training.

The courses offered by Intellipaat address the unique needs of working professionals. She is based out of Bangalore and has an experience of 5 years in the field of content writing and blogging. Her work has been published on various sites related to Big Data Online Training, Business Intelligence, Project Management, Cloud Computing, IT, SAP, Project Management and more.

Publication date

Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not reflect the views of Bitcoin Insider. Every investment and trading move involves risk - this is especially true for cryptocurrencies given their volatility. We strongly advise our readers to conduct their own research when making a decision.