Latest news about Bitcoin and all cryptocurrencies. Your daily crypto news habit.

This is an extract from an upcoming paper in the Journal of Payments Strategy and Systems.

The Blockchain and its Limitations

While most in the cryptocurrency and blockchain space agree that open public blockchains are likely the future of “transaction of value”, many also agree that we are a long way before this infrastructure is at a level that can effectively support even a fraction of the world’s commercial economic activity.

There are a number of limitations that make current open public blockchain networks unfeasible for wider commercial use. Some of the key ones, that are part of ongoing research and development efforts, include network latency (time taken to include blocks into the blockchain) and throughput (number of transactions that can be included in a block at any one time). For example, Bitcoin latency is ~10 minutes and has an average throughput of ~5 transactions per second (tps), while Ethereum has latency of ~15 seconds and an average throughput of~20tps. However, latency can be even longer during peak times, as new transactions are queued and prioritised based on size and fees. As a benchmark, these throughput numbers pale in comparison to Visa’s ~2,000 tps.

Apart from processing capability limitations there are other operational aspects that require further research. For example, the energy required to secure a blockchain through PoW [1] and the storage requirements for every full node participant in the network to keep a copy of all the transactions that were ever processed, which currently stands at ~180gigabytes for Bitcoin and ~325gigabytes for Ethereum [2].

We won’t go into further details on the above mentioned technical challenges, as the focus of this discussion is on privacy on open public blockchains. One of the key aspects of an open public blockchain is that cryptocurrency payments and any associated secondary token issuances/transfers are recorded transparently in the blockchain ledger. Which means anyone, who knows your public address, can see and track your economic activity. Thus, if you are using an open public blockchain for financial transactions, such as issuing a bond, the flow of funds and ownership of securities would be publicly available information!

In its current form the consensus mechanism used in Bitcoin and Ethereum requires extreme transparency to ensure any network participant can access all the required data to validate and record transaction and enable the network to converge to the true state of the system. Transparency is so important to reach consensus that, to some degree, individual privacy is sacrificed. However, as long as users keep their public addresses confidential they are able to manage a certain level of privacy, known as pseudo-anonymity, but this is challenging over an extended period and makes current public blockchains unviable for most commercial financial services applications.

Transparency vs Privacy

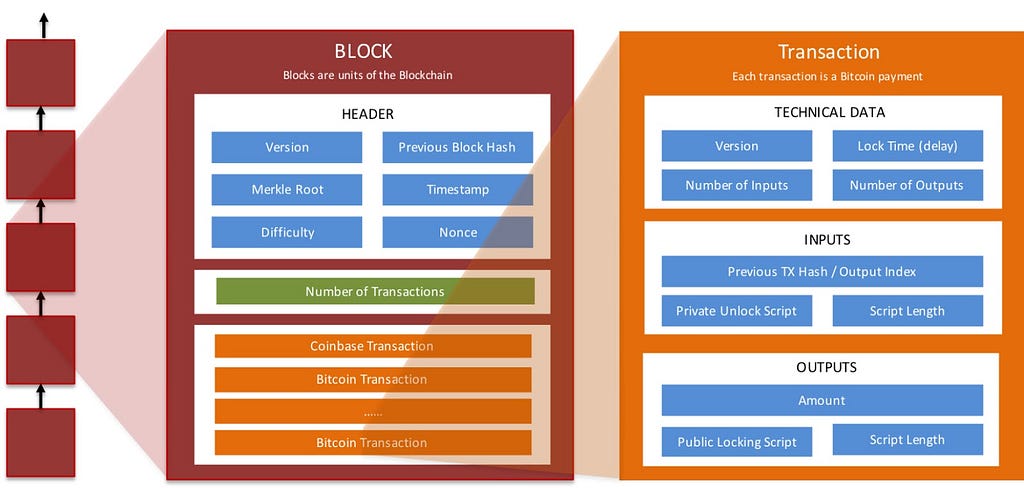

One of the key aspects that makes the concept of a decentralised ledger technically viable is that all transactions are open for everyone to see on the network. This transparency means that anyone can validate if a particular transaction and the encompassing blocks follow the network’s protocol rules. The three key aspects for validation are as follows:

- Economic: sender has enough tokens to send as part of the transaction

- Security: sender can prove they own (or have access) to the tokens they are transacting

- Structural: blocks are appropriately structured and are part of longest chain

The network consensus model leverages the transparency of the transmitted transactions so they can be reviewed, validated and “mined” into the blockchain ledger, in addition every mined block that is shared across the network can be validated and included to the end of the chain. This means that every transaction that is ever sent, and the value being sent is available for all to see, and more importantly anyone can use this information to participate in the use of the network or the process of securing the network i.e. validating new transactions and forming new blocks.

The issues with such transparency is that it can easily be used to infringe on an individual’s privacy, both in terms of tracking payments made in the network’s cryptocurrency and also tracking ownership of secondary tokens that are used to represent rights to other issued assets such as securities.

This extreme level of transparency would be equivalent to having your bank account number and all the transactions you ever executed being available for everyone to see. If someone knew your account details they could track your entire financial history. This brings us to the point of privacy. As long as you keep your account number, or blockchain address in the case of bitcoin/ether, a secret you can try and abstract the flow of funds i.e. as noted above achieve a level of pseudo-anonymity. However, doing so would be troublesome, and over a period of time is not very effective.

We can then ask the natural but complex question: are the two factors — the need for transparency to drive the consensus mechanism and right to privacy for individuals — incompatible in a decentralised world? Do we have to sacrifice one to enforce the other?

Transparency and Privacy as Social Constructs

There is much debate, both legally and socially, around the correct balance to strike between an individual’s, organisation’s or state’s need for privacy and the need for transparency. Data protection laws typically assure a certain amount of privacy with the need for transparency being assured by freedom of information laws which are, increasingly, a part of national laws for developed democratic countries as a means of holding governments to account and tackling the imbalance of power between states and citizens.

While using transparency as a means to hold power accountable is a fundamental tool against corruption and exploitation, its balance against the loss of individual’s privacy is an important consideration.

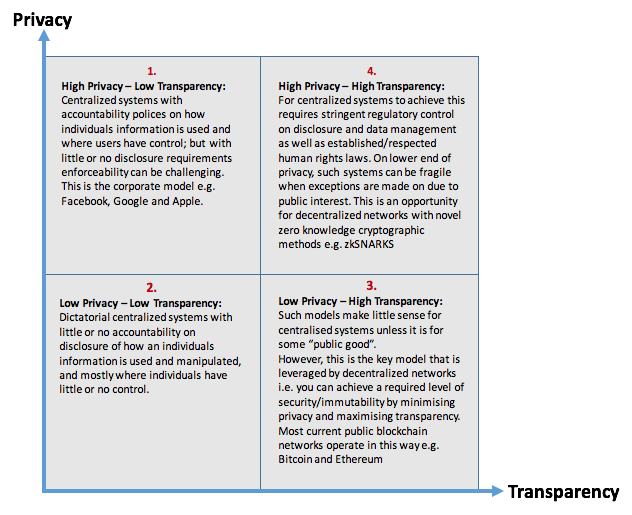

As shown in Figure 2, while a balance between privacy and transparency is challenging it can be managed in centralized systems through the use of regulations and national/international laws. However, these do leave room for abuse by self interested organisations and governments. While decentralized systems may mitigate the risks of concentration and abuse of power, this currently comes at the loss of privacy for the individual.

Sacrificing Privacy for Consensus

When we move away from a centralised systems it is difficult to pinpoint where accountability should sit as there is no single authority that could be responsible to maintain the system correctly/honestly and be accountable for privacy of users data. In particular, in an open public blockchain infrastructure new nodes, or those maintaining the network through validation and mining, can come and go dynamically, and anyone is able to participate in the mining process to secure the network just by adding computing power. In such a decentralised setup the accountability lies with all the participants, hence the need for a consensus mechanism to coordinate and converge to the truth. This is where the extreme transparency of transactions on the blockchain are required, to ensure that all the participants can see exactly what was transacted, how it was transacted, and what the current state of the ledger is. This way all the participants of the network can compete to converge to the “true” state of the ledger of transactions — using the same rules and with equal access to data. To enable this system to function all participants need to not only have equal access to information but also see all the details of every transaction and the history of the blockchain to be able to validate and mine new transactions into the chain.

As long as users are ok with sharing all their economic history and future activity over an open public peer-to-peer network such a model works well. However, when the information is financially sensitive e.g. a user’s bank account and investment portfolio, the lack of privacy can be an issue and point of friction for wider commercial uptake.

Overcoming Privacy Challenges

The current lack of privacy is not a complete deadend, as noted earlier open public blockchain infrastructure is in its infancy. While tried and tested cryptographic tools underpin current frameworks, such as public key cryptography and hash functions, there are a number of novel concepts/tools that are undergoing industry experimentation that may be the holy grail for balancing the need for transparency with a desire for privacy. One of these cryptographic concepts is Zero Knowledge Proofs, and a specific implementation of this is known as zk-SNARKs[3][4], which is used by the privacy focused cryptocurrency Zcash [5].

In general zero-knowledge proofs allow one entity, the prover, to prove to another entity, the verifier, that a statement is true, without revealing any information beyond the validity of the statement itself. Traditional zero-knowledge proofs may require interaction and sharing of information back and forth between a prover and verifier for multiple rounds. However, non-interactive zero-knowledge proofs (i.e. zk-SNARKs) are a variant in which only a single message, or “proof”, needs to be shared between the prover and verifier.

Without going into the technical details, as an example, imagine you have hashed a number and you want to prove to another person you know what the number is without revealing it. Using a zero knowledge proof you could convince the verifier that there indeed is a number with this hash value and you know this number, without revealing what the number is. This can be achieved with zero-knowledge proofs. So in general you can leverage such privacy tools to prove certain steps have been taken in a transaction without revealing what those steps actually are i.e. only reveal part of the process without showing the whole process itself and prove that you are being honest about your claims.

Such zero-knowledge proofs can provide assurances that users are only spending money that they have without revealing on the public ledger who they are and how much they have received or sent to others. In Bitcoin, transactions are validated by linking the sender address, receiver address, and bitcoin input and output values on the public blockchain, which can be openly seen by all parties i.e. are transparent. In the case for Zcash, it uses ZK-SNARKs to prove that the conditions for a valid transaction have been satisfied without revealing any crucial information about the addresses or values involved. The sender can construct a “shielded” transaction proof to show that the economic, security and structural consensus rules (discussed above) have been followed.

Thus, using such cryptographic tools, one can maintain the required transparency to ensure the network consensus rules have been followed, but the underlying information of who sent how much to whom would remain private.

However, it is critical to note that such Zero Knowledge cryptographic privacy tools are highly novel. There are a number of challenges related to the current setup processes, performance and even future consequences when the tools are compromised and immutable private transactions would become visible.

This is just the Beginning

While we have highlighted some of the technical challenges that underpin the use and wider adoption of cryptocurrencies and open public blockchains, an important point to note is that we are only at the very early stages of the use of this technology.

While the industry will likely experience significant challenges due to inflated cryptocurrency prices and legal/regulatory challenges, the chances are that some variant of this technology will likely form the basis of future payments and asset clearing and settlement systems. Dismissing cryptocurrencies and the technical and economic innovations that underpin them merely due to the current challenges and limitations would be like dismissing the internet in the early 90s just because you couldn’t deploy Netflix on the infrastructure at that time.

To receive thoughts, discussions and papers on finance, economics, law and the human condition follow on twitter: @avtarsehra

Thanks to Richard Cohen and Vic Arulchandran for their input and support of this work.

Publication date

Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not reflect the views of Bitcoin Insider. Every investment and trading move involves risk - this is especially true for cryptocurrencies given their volatility. We strongly advise our readers to conduct their own research when making a decision.