Latest news about Bitcoin and all cryptocurrencies. Your daily crypto news habit.

Competitive Analysis of the Liquid Staking Options on the Ethereum Ecosystem

Major advantages and disadvantages from the top liquid staking derivatives prior to the Shanghai fork

The Ethereum merge was among the most notable achievements for the crypto space in 2022. This phase marked Ethereum’s network transition into a proof of stake consensus, which so far has received wide adoption, reaching a total of almost 16 million ETH staked. This number nearly doubled since the beginning of 2022, making it more costly to attempt to attack the network while economically aligning validators’ incentives with Ethereum’s long-term growth.

Liquid Staking Derivatives (LSD), can be in part attributed to the growth of ETH staked in the network. For those still not familiar with the concept, LSDs allow a different way for users to stake their ETH. As its name implies its a derivative that represents the ETH locked in the staking contract. This innovation contributed to making the staking process more easy and accessible. It has enabled users to participate in the proof of stake mechanism without permanently locking their capital or having to reach the high minimum deposit of 32 ETH. Additionally, LSD tokens provide further utility to staked assets, it opens interactions with DeFi’s protocols allowing staked tokens to be deposited as collateral or liquidity provision.

The next significant upgrade in line for the Ethereum network is the Shanghai fork, which will allow those staking to progressively unlock their locked ETH from the stacking contract. This can potentially bring large second order effects for ETH, LSDs and entities staking ETH. While the Shanghai fork will open the possibility of withdrawing locked ETH, it could also lead many more to stake bringing a higher attention to the current LSD options. This article aims to analyze some of the current LSD options, their benefits and challenges for their continued protocol growth.

Lido’s stETH

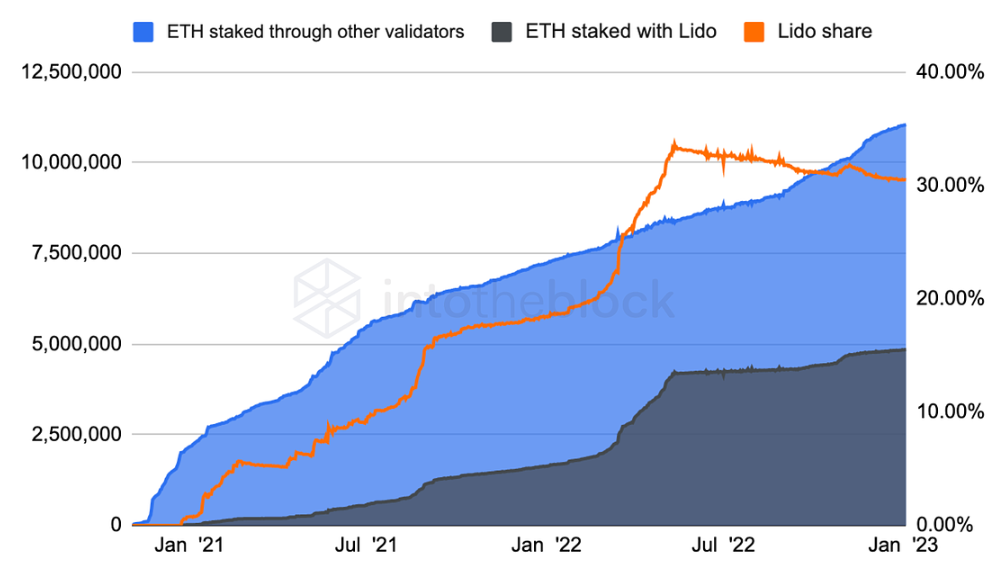

Lido currently stands as the major staking service provider, managing a total of 29% of the total ETH staked. Their model is simple, users provide ETH to be staked in return obtaining stETH and then Lido directs users ETH into staking institutions for it to be staked into the Ethereum network. For this service Lido charges a 10% fee on staking rewards that are split between node operators and the DAO Treasury.

Data based on IntoTheBlock’s Ethereum staking and stETH supply metrics

Being the first and most straightforward system for liquid staking, it has managed to receive great adoption across the DeFi ecosystem. In total users have staked 4.8 million ETH through Lido (~$5.8 billion). Their main gateway to open liquidity for users staking is through the Curve protocol, having the top pool of the protocol by TVL be stETH-ETH, this high liquidity gives higher trust for depositors.

One disadvantage that the protocol could face could be that its model does not offer any alternatives for people seeking to gain more than the regular staking yield. This could represent a threat as new models emerge and the Shanghai fork makes it easier for arbitrageurs to keep liquid staking tokens at their value. The lack of an alternative with higher yield could potentially take market share away from Lido in the future.

Rocket Pool’s rETH

This project stands out as the most in line with traditional crypto ethos in the Ethereum ecosystem. Their goal is to create a decentralized ethereum staking mechanism by uniting independent node operators with ETH stakers. Currently to run a Rocket Pool node only 16 ETH are needed instead of the original 32 ETH required. The other 16 ETH needed to set up the full running node are provided by the rETH liquid stakers.

In this way rETH stakers accrue rewards over time and pay a commission to the Rocket Pool node operators, which in turn end up earning a higher yield on their tokens than the regular staking yield. Rocket Pool charges a 15% commission to liquid stakers, which is fully directed to its node operators.

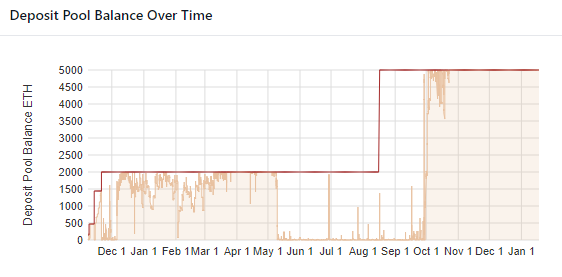

Source: Rocket Pool Explorer

While rETH liquid stakers wait for a willing Rocket Pool node validator to be set up with their tokens they are held up on to the protocols “Deposit Pool”. There is a limit to the amount of ETH that can be in the deposit pool at any given time, currently being 5000 ETH. While its full, no further liquid staking deposits are accepted; rETH can only be obtained by purchasing it in the open market. On the other hand a problem can be presented if users are not willing to simply liquid stake, in which a line of waiting node validators is formed until users willing to liquid stake with rETH are found.

Currently Rocket Pool’s share of total ETH staked on the Ethereum network stands at 2.2%. They keep attracting rETH liquid stakers by incentivizing DeFi pools, like their Aura WETH-rETH pool. Among their biggest growth facing challenges stands the ability to attract willing node validators operators, the protocols Deposit Pool has been full now for over two months. Here the Rocket Pool protocol is trading off scalability for greater decentralization.

Frax’s frxETH and sfrxETH

This DeFi protocol offers an array of products, including two stablecoins (FRAX + FPI), a decentralized exchange (Fraxswap), a lending protocol (Fraxlend), and a bridge (Fraxferry). With this vast experience the team came up with a pretty interesting token engineering model. ETH in the Frax ecosystem comes in two forms, frxETH (Frax Ether), and sfrxETH (Staked Frax Ether). This two token implementation comes as a variation to the Stakewise and Ankr protocols model used before.

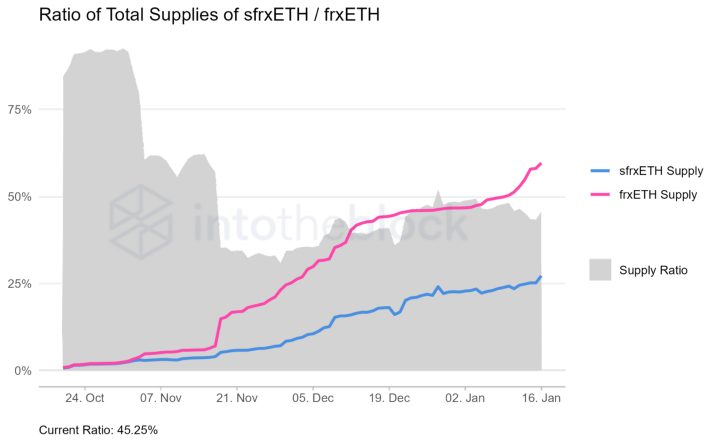

Historical ratio of total supplies of frxETH and sfrxETH according to IntoTheBlock Research.

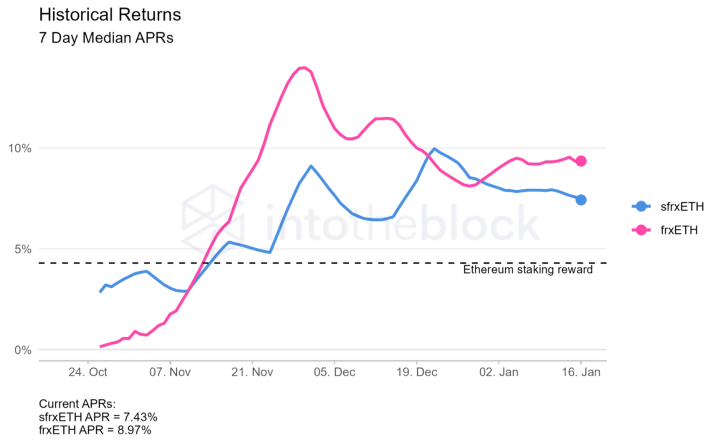

frxETH targets to be loosely pegged to ETH. Holding frxETH on its own is not eligible for staking yield. frxETH can be exchanged for sfrxETH by depositing it into the sfrxETH vault. Over time, as validators accrue staking yield, an equivalent amount of frxETH is minted and added to the vault. This allows users to redeem their sfrxETH for a greater amount of frxETH than they deposited, meaning all the staking yield generated by the frxETH holders only goes to those that exchanged it for sfrxETH.

Since frxETH holders don’t earn rewards, but do contribute to the staking platform, sfrxETH holders gain a higher APR than other staking derivatives. The reason for this increased return is because while all frxETH minted ends up locked in the validator contract, not all the frxETH holders decide to stake. Currently the other main use case for frxETH holders is to deposit in the Curve’s WETH-frxETH pool since it’s directly incentivized by the Frax protocol its yield is more attractive than the sfrxETH staking rewards.

Historical 7 day median APRs for frxETH and sfrxETH according to IntoTheBlock Research

The first graph shown above in the Frax section shows the ratio for users that exchanged their frxETH for the version of the token that accrues staking yields sfrxETH. The second graph shows the historical APY returns for both versions of the asset. A rate close to 100% in the first graph means that most frxETH is staked as sfrxETH. This will limit the exit liquidity available in their frxETH-ETH Curve pool and in addition the APY offered to sfrxETH holders would be similar to other staking options since there would not be additional ETH staked for the sfrxETH holders, potentially eliminating their competitive advantage.

In this scenario the biggest challenge that the protocol could face is to keep the demand and utility for frxETH high, so that not everyone ends up switching into sfrxETH. They can achieve this by either integrating frxETH deeply into the Frax ecosystem or by continuing to incentivize the Convex pool so that yields remain attractive.

Conclusion

The Shanghai fork represents a great milestone for the Ethereum community, which will shed light into the developing liquid staking environment. The fact that people staking will soon be able to withdraw, even if they have to form part of a waiting queue, could in turn encourage more people to stake earn yield and contribute to the network’s security. Out of the proof of stake networks, Ethereum currently holds the lowest percentage of circulating supply staked; the Shanghai fork could change users views and become more comfortable staking ETH.

Finally, this article summarizes some of the upcoming trends in the LSD environment, their major advantages and weaknesses. There are still other interesting innovations like Coinbase, also the second largest entity staking, cbETH worth exploring if interested in further research. As for a 2023 outlook, if an increase in the amount of ETH staked does materialize, liquid staking services such as Lido, Rocket Pool and Frax ETH are expected to record increasing revenues. This explains the growing attention towards the specific sector.

Competitive Analysis of the Liquid Staking

Options on the Ethereum Ecosystem was originally published in IntoTheBlock on Medium, where people are continuing the conversation by highlighting and responding to this story.

Publication date

Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not reflect the views of Bitcoin Insider. Every investment and trading move involves risk - this is especially true for cryptocurrencies given their volatility. We strongly advise our readers to conduct their own research when making a decision.