Latest news about Bitcoin and all cryptocurrencies. Your daily crypto news habit.

The two biggest obstacles for startup founders.“Venture services focuses on solving a specific sub-section of founder needs: the need for quality software and the need for capital to pay for it.”

The two biggest obstacles for startup founders.“Venture services focuses on solving a specific sub-section of founder needs: the need for quality software and the need for capital to pay for it.”

This post is the second part in a series on venture and venturing. Part One examined the ‘what’ and the ‘why’ of venture, primarily from the perspective of the providers.

This second part deep dives into ‘how’ venturing actually works in the context of venture services, the corner of the venture ecosystem I occupy as a partner of London-based Pivot Venture Services.

My first experience of venture was via PreHype, a pioneer of the corporate venture model. PreHype facilitate a number of innovation programmes globally and, in collaboration with NewsCorp, helped birth Newsmart, for whom I was Product Director in 2015.

My first real break in venture came as MD for Castle (aka ‘Castle Digital Partners’), a venture services firm based in Charlotte, NC. I set up Castle’s London Studio and inked their first European venture deals.

Venture, in all its forms, is the professionalisation of angel investing.

Angel investment has a bad reputation. One that is characterised by chaos, amateurism and exceptionally high levels of risk.

I once attended an investment seminar where a seasoned angel presented the view that one shouldn’t expect to make any money from angel investing and that it was more about having fun.

This seemed counter-intuitive. But when your company is you, a big idea and a slidedeck, it’s hard to convince others to back you (especially if you’ve never started a company before.) Given the obstacles, its a miracle first-time founders ever make it out the gate.

Super-early startups are a ‘dead-zone’ analytically. Valuations, forecasts, market sizes and business plans are like Shrodinger’s Cat; simultaneously worth zero and one million.

An early-stage startup valuation.

An early-stage startup valuation.

Institutional investors don’t engage until much later on. They are scaleup, as opposed to startup, investors. They enjoy the comparative luxury of a working product, market traction, even revenue from the companies in which they invest.

What is Venture Services?

Venture services firms serve two sets of interests, those of early-stage founders and of early-stage (‘angel’) investors. They facilitate transactions that align the interests of both towards the rapid creation of equity value.

Jeff Bezos is well known for advising founders to ‘bet on the things that don’t change’ if they want to build a durable business. He bet on customers’ desire for low prices and fast delivery not changing and both seem to have paid off well.

For venture services firms, the bets are as follows:

- We are betting that startup founders will continue to need capital and great quality software.

- We are betting that wealthy individuals will increasingly want to invest in startups whilst reducing the risk of losing their investment. (In the UK in particular, they will continue to take advantage of the UK Government’s generous tax relief schemes, such as SEIS and EIS, for as long as they are available. More on this later…)

Bet #1: Founders

Proptech. Lawtech. Connected Enterprise. Smart Cities. IoT. The tech-sector is diversifying rapidly. And so is the archetypal startup founder.

Outside of Silicon Valley, it’s increasingly rare for first time founders to be hackers or coders. Instead, most are domain experts who have identified an opportunity to disrupt or transform the status quo with software. They are, in the words of Paul Graham, “just some business person.”

And for “just some business person” with a vision but no technical experience, the challenge of building an initial product and finding sufficient capital to pay for it can be insurmountable. It’s a much greater obstacle to startup progress than is commonly acknowledged.

Historically, non-technical founders looking to start a company have had two options to choose from.

Either they find a technical co-founder / CTO and rely on them to build a product in exchange for a healthy slice of equity.

Or they reach further outwards to one of the many providers of software services (aka ‘dev shops’), typically located on the eastern edge of the European Union (think Poland, Czechia, Belarus, Ukraine, Russia), or in India and pay them in cash.

Each route has its pros and cons, both of which have been well documented here and here.

Venture services firms offer a third option to founders, one that sits between an invested employee and a detached supplier. And one which, ideally, offers the benefits of both.

These firms don’t create companies or lay claim to their ideation. They partner with mission-driven founders to solve a specific subsection of their needs: the need for working software and the need for capital to pay for it.

For startup founders, finding a partner willing to remove the two biggest obstacles to early-stage progress can be compelling. It’s common to hear founders talk of their desire for value-added capital. Done correctly, venture services should feel like an accelerator on steroids.

By trading in equity, venture services firms attain goal congruence with founders that suppliers are unable to achieve. This creates a partnership culture of trust and shared outcomes.

What’s most appealing to investors, however, is that venture services significantly reduces risk. This includes team risk, technical risk and (above all) execution risk at pre-product stage.

The percentage of startups who burn through their initial capital but fail to deliver an actual product remains surprisingly high. This usually occurs when CEOs unexpectedly part company with their CTO and find themselves with half a product that has little or no value.

Experienced angels will have witnessed this on multiple occasions. Having confidence that a product will be delivered, on time and on budget, is rare and appealing.

Bet #2: Investors

Investment decisions don’t exist in a vacuum. They occur within a complex macro-economic environment of financial incentives and opportunities, notably tax relief and grant-funding.

All governments seek economic growth. As startups are high-growth vehicles by definition, governments are increasingly trying to incentivise early-stage investment. Widespread awareness of the generosity of these schemes, combined with the explosion of interest in startups, has created a perfect storm of capital searching for a home.

By way of example, let’s examine the UK government’s Seed Enterprise Investment Scheme, better known as SEIS. For early-stage startups, SEIS is the financial equivalent of methamphetamine.

In the words of CrowdCube,

“To say that the Seed Enterprise Investment Scheme, or SEIS, is incredibly generous is somewhat of an understatement. Of course we all hope our investments do well, but if you pay tax at 45% and make an investment of £10,000 that fails completely, you only lose £2,750 due to the tax relief.”

Wealthy individuals with high income tax bills have stampeded to find startups that will allow them to take advantage of the tax relief offered by SEIS. But few have direct access to qualifying companies or the time to find them.

Whilst the relief is an end in itself, investors also want to protect their investment and minimise downside potential. They’re not just looking for startups that qualify for SEIS tax-relief. They’re looking for the best startups that qualify for SEIS tax-relief.

Via access to select early-stage startups, venture firms are well positioned to broker these trades.

How Venture Services works

In Part One, I observed that the economic details of venture deals are rarely disclosed. It’s hard to quantify how much equity (and cash) really changes hands between founders and venture firms. The spectrum is very broad.

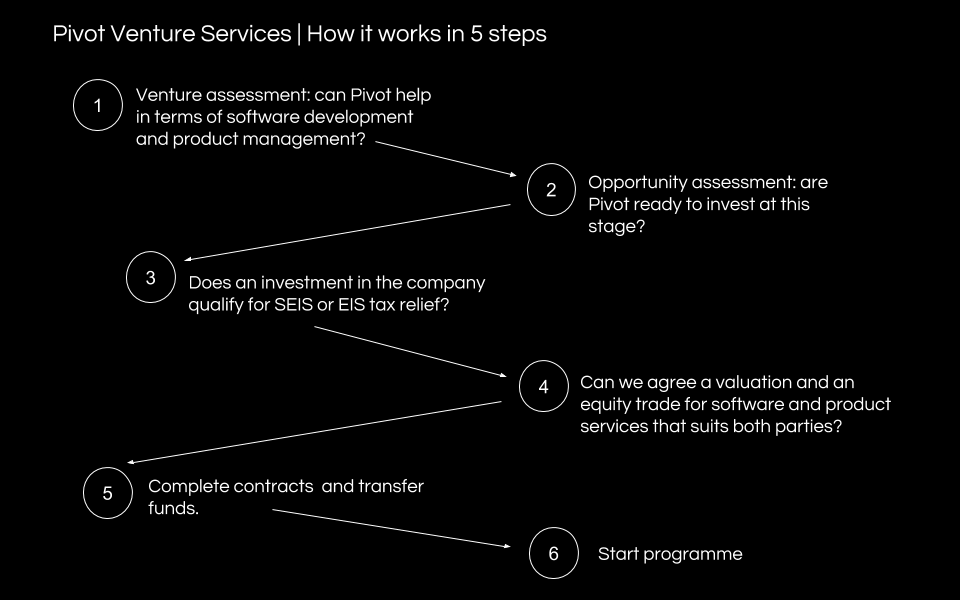

As a first stab at demystification, below is a breakdown of how a successful venture engagement works at Pivot. It’s a happy path, one in which all the boxes are checked.

The very short summary is that venture services means building software in exchange for equity, syndicating part of the equity to cover costs, and retaining the remainder as margin. This aligns the firm’s incentives and upside with those of the founder(s) with whom they partner.

The slightly longer version is as follows:

- The firm meets a startup founder and makes an investment decision based on the market opportunity and the extent to which quality software will create momentum and initial traction.

- Working closely with the founder(s), the firm scopes and estimates the cost of the software development required to help the startup reach its agreed goals.

- The firm’s Investment Manager determines if additional cash is necessary and calculates the equity premium the firm will add as margin.

- The firm agrees a pre-money valuation with the founder(s) and makes a proposal to develop their software in exchange for a % of the equity in the company.

- If both parties agree to terms of the venture proposal, the founder(s) transfer the agreed equity to the firm, typically via an option or an Advanced Subscription Agreement (ASA).

- The venture firm designs, develops and deploys the agreed software for the startup and maintains/iterates upon it for an agreed period of time. The software engineering team are paid directly by the venture firm from their fund capital or by syndicating a % of the equity to investors in exchange for cash.

Why Venture Services is Hard

Why Venture Services is Hard

Compared to other forms of venture capital, venture remains niche.

This is primarily due to the complexity of the business model. There are more moving parts, and more factors to align, in a successful venture deal than a conventional investment. Most investors prefer to avoid the additional overheads and responsibilities of being a venture partner.

Additional reasons I have observed are as follows:

#1: Cashflow

In Part One, we explored why venturing can’t be funded by profits from a services business; at least not long-term.

Services businesses generate revenue in the form of cash. Venturing is investing, which is deferred revenue. What makes the two irreconcilable is usually the cost base.

As software companies are asset-light, the lion’s share of their cost base is payroll. If you have a lot of salaries to pay at the end of each month then you need the cash to pay them. And, if all of your profits are funding ventures, then you are dangerously exposed in a downturn.

I have experienced services companies with large workforces all but go bankrupt trying to move into venture. The consequences were drastic and unfortunate, mainly for the employees.

So, how can venture firms build software without the overhead of large team of developers and designers? We solve for this at Pivot by mobilising teams on a deal-by-deal basis and work within a tightly managed, fixed cost environment.

We generally employ a mixed model, with CPO and CTO working ‘onshore’ (in our case, in London) and UX, design and engineering working ‘near shore’, typically in Eastern Europe. We always seek to build long term partnerships by working with the same individuals across a number of ventures. This creates bonds of familiarity and trust that generate real team effectiveness over time.

The costs for the team are rolled into the overall capital raised by the venture firm and then exchanged for equity in the company.

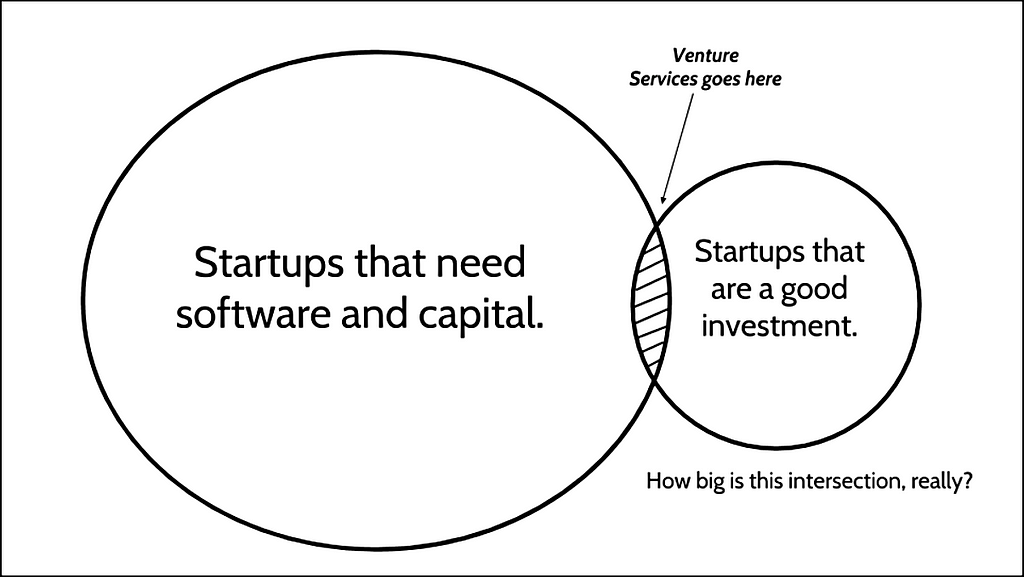

#2: Market-size

Finding startups that are good investments is hard. Finding startups that are pre-product, pre-revenue and a good investment is a treasure hunt of mythical proportions.

It’s hard to accurately size the market for venture services. It could be very small based on the ratio of deals we have done versus the opportunities we have passed on.

The downside of working at the highest risk end of the investment spectrum is that it’s, well, risky. Most investors prefer to see proof of market traction. It’s a giant leap of faith to invest in a market for something that doesn’t yet exist.

Pivot endeavours to de-risk this by backing founders who sell back into their primary network, at least in the first instance.

Ex-lawyers are well positioned to sell lawtech solutions to other lawyers. Ex-marketers selling marketing platforms to their former (marketing) colleagues is a reasonable bet. Unlike hackers, “just some business person” often has the edge when it comes to sales. And sales is the bigger challenge long-term.

#3: Culture

Venture services firms combine expertise (and application) in two distinct fields: early-stage investment and software product development. Folks from these respective fields come from different places, have different mindsets and speak different languages.

Service providers are instinctively inclined to work with whoever wants to work with them. Investors are instinctively sceptical. Service providers are default ‘yes.’ Investors are default ‘no’.

I speak from experience when I say that the two are also treated very differently by founders and the startup community in general.

Investors are top of the food chain and get treated accordingly. They enjoy high response rates to their emails and meeting requests. They don’t sell or hustle as a rule.

Life is different for providers of software services. Much of their time is taken up writing estimates and proposals that go unacknowledged. Their communications are ignored. They have to hustle constantly.

Part of the achievement of a venture services firm is finding a common ground for these very different individuals to interact within. This alone is a barrier to entry.

TL:DR

That’s pretty much all I have to share, so far. As you can probably tell, I’m bullish about the potential of venture (and venture services) as an emerging category within venture capital as a whole.

Any other players (or aspiring players) within the space, I’d love to hear from you.

Here’s the TL:DR:

- Venture is still a niche space, primarily due to the complexity of its business model.

- All equity deals (ie. where startups pay no cash) are the most compelling, differentiated, and potentially lucrative form of venture. Smart founders value the opportunity to onboard an experienced product team at speed and are prepared to trade their equity accordingly.

- It’s impossible to succeed in venture without access to a pool of capital, typically a fund or syndicate of investors.

- Keeping overheads as low as possible is key to success.

- Whilst the value proposition is compelling and the problem large and frequent, the size of the addressable market remains hard to quantify (and may be very small.)

On Venture Services was originally published in Hacker Noon on Medium, where people are continuing the conversation by highlighting and responding to this story.

Publication date

Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not reflect the views of Bitcoin Insider. Every investment and trading move involves risk - this is especially true for cryptocurrencies given their volatility. We strongly advise our readers to conduct their own research when making a decision.