Latest news about Bitcoin and all cryptocurrencies. Your daily crypto news habit.

Disclosures continues to be one of the existential challenges to the security token industry. In a market without any information about active digital securities, the opportunities for achieving fair trading remain very limited and that dynamic gets worse as the market growths.

When comes to security tokens, disclosures is not a problem with a unique solution. Quite the opposite, there are numerous models that can be applied to enable better information flow for digital securities . In the past, I’ve outlined some ideas about the challenge of disclosures in security tokens. Today, I would like to propose four different models that might help to tackle this challenge for both basic and really sophisticated scenarios.

It is natural to think about disclosures as an information flow problem but I think that perspective results constrained when comes to security tokens. After all, asset classes like cryptocurrencies also lack a trusted information flow and they seem to maintain price fairness across different market cycles.

A more complete way to think about the disclosure challenge is as a combination of two phenomenon’s in crypto-asset markets: information asymmetry and decentralization.

Information Asymmetry vs. Decentralization

In economics, information asymmetry describes a market dynamics in which different parties involved in a transaction have a disproportional level of knowledge relevant to the exchange. The term was made famous by Nobel Prize Winner George Akerlof in his essay “The Market for Lemons” in which he uses a picturesque example to drive the thesis that markets with asymmetric information between buyers and sellers might never achieved fair pricing (I’ve written about Akerlof’s theory before so I would like to use other examples today 😉).

Despite what we might think of, information asymmetry is a very common phenomenon in different markets. The insurance industry is a classic example of an industry that knows how to capitalize on asymmetric information flows.

Over the years, there have numerous studies that showed very little positive correlation between insurance and risk occurrence in real markets. One possible explanation for this is that individuals do not have more information about their risk type, while insurance companies have actuarial life tables and significantly more experience.

Another foundational analysis about asymmetric information in mainstream markets was published by economists Michael Spence in his 1973 paper titled “Job Market Signaling”. In his essay, Spence models employees as “uncertain investments” for companies as they can’t quite predict their productivity in advance.

Spence proposed that two parties could get around the problem of asymmetric information by having one party send a signal that would reveal some piece of relevant information to the other party which will interpret the signal and adjust the pricing accordingly.

A final theory that is relevant to understand information asymmetry is the Screening model pioneered by American economist Joseph E. Stiglitz. Across several research papers, Stiglitz proposed the idea of using screening games that allow the parties with less information in a transaction to mitigate that risk.

For instance, a typical screening game in our job market scenario might for an employer seeking a salesperson may offer a contract with a low base salary supplemented with a commission when sales are made.

Information asymmetry is the source of many inefficiencies in economic markets and, under certain circumstances, it can become a roadblock for fair trade. An important distinction to make is that information asymmetry behaves differently in centralized or decentralized ecosystems. In centralized environments in which a handful of parties have the access to all relevant information for a transaction, the negative effects of information asymmetry are accentuated by the constrained flow of information.

However, in large decentralized markets, the behavior of the participants mitigates some of the vulnerabilities of information asymmetry. Effectively, in sufficiently decentralized ecosystems, price fairness is achieved by the behavior of the participants in the network and not so much by the flow of information. In a decentralized ecosystem, any unfair behavior will be balanced by other network actors without having to rely on a centralized authority. In that sense, information disclosures are not as important in a sufficiently decentralized ecosystem as they are in centralized markets.

If think about security tokens in the context of the information asymmetry and decentralization vectors we find a scary picture. Digital securities are not only fairly centralized in terms of its transaction model but also incredibly asymmetrical in terms of information flow which makes it incredibly vulnerable to market manipulations.

Four Models to Address Disclosures in Security Tokens

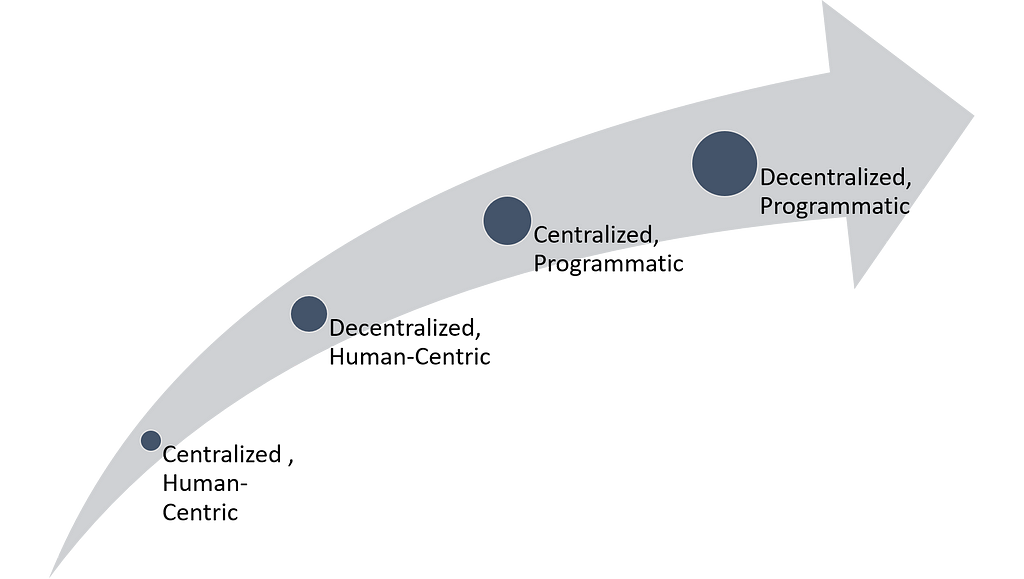

The disclosure challenge for security tokens is a problem that needs to be tackled in multiple phases. In an immature and inefficient market like digital securities, disclosure models need to evolve in parallel to the sophistication of the digital assets themselves. In a short-to-medium horizon, we can model four incremental solutions to enable disclosures in digital securities.

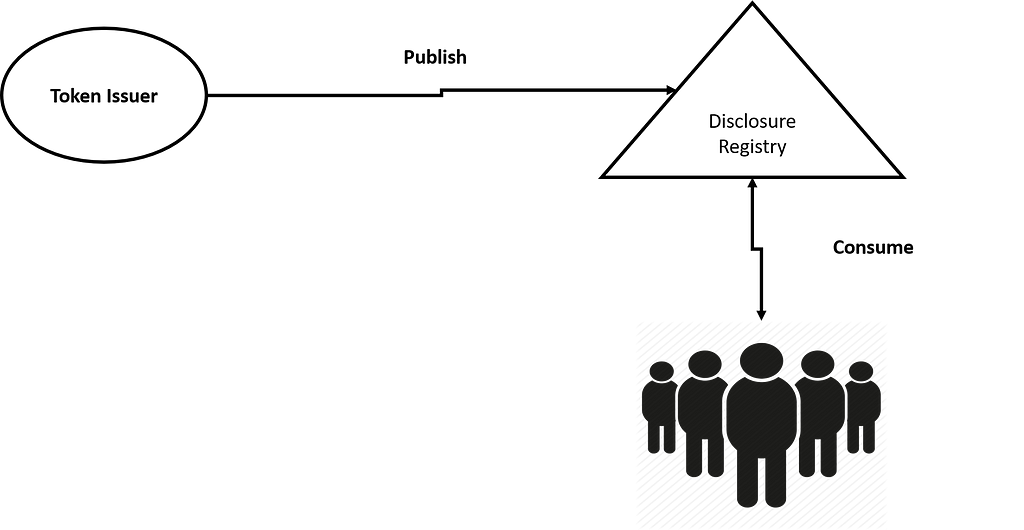

Centralized, Human-Centric Disclosures

Centralized, Human-Centric Disclosures

This is the traditional model in which information provider such as token issuers will publish relevant information to a centralized repository which can be accessed by token holders and other relevant parties.

This model assumes an intrinsic trust on the information publishers and centralizes the access to the disclosures. Furthermore, the disclosures are intended to be consumed by token holders in order to make future investment decisions.

Decentralized, Human-Centric Disclosures

Decentralized, Human-Centric Disclosures

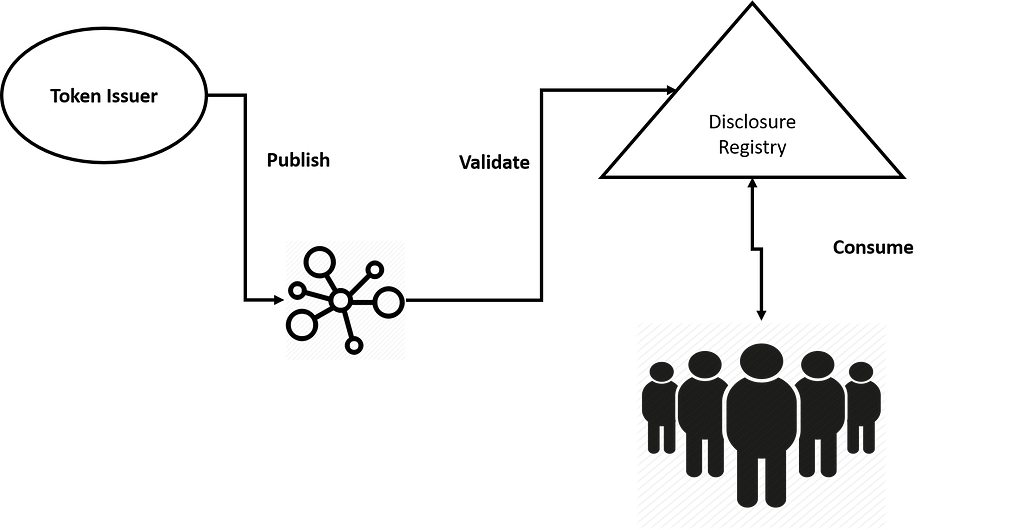

This model represents an incremental improvement over the previous architecture by decentralizing the validation of the information. Similar to the previous dynamic, token issuers or other information providers will publish material information about a specific digital security.

However, this model will rely on a network of validators to assert the correctness of the information before is available to the token holders. This model maintains the human-centric consumption of the disclosures but introduces a decentralization vector for its validation.

Centralized, Programmatic Disclosures

Centralized, Programmatic Disclosures

This model transitions disclosures to programmable protocols that can be directly used in blockchain applications. The main idea behind this concept is that disclosures would not only be used by humans but also via programmatic interactions at the protocol level.

In this model, security tokens will programmatically access and distribute disclosures that can influence the outcome of a specific transaction. The flow of information remains centralized as is mostly controlled by the issuers, but the interactions transition from humans to applications.

Decentralized, Programmatic Disclosures

Decentralized, Programmatic Disclosures

Arguably, the ultimate manifestation of disclosures in security tokens, this model proposes both programmatic and decentralized interactions for information publishing. In this model, information providers will distribute relevant information via a disclosures protocol which will be then validated by other nodes in the network.

Solving the disclosure challenge for security tokens is going to be a long and iterative process but we need to start somewhere. The longer the digital securities market evolves without any flow of information, the longer it will accumulate inefficiencies to a point that might not be solvable. Hopefully some of the ideas outlined in this article will be relevant to enable the first generation of disclosure models for security tokens.

Four Ideas to Enable Disclosures for Security Tokens was originally published in Hacker Noon on Medium, where people are continuing the conversation by highlighting and responding to this story.

Publication date

Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not reflect the views of Bitcoin Insider. Every investment and trading move involves risk - this is especially true for cryptocurrencies given their volatility. We strongly advise our readers to conduct their own research when making a decision.