Latest news about Bitcoin and all cryptocurrencies. Your daily crypto news habit.

Ranking crypto-economies, pricing the disintermediation of trust, and the true sources of intrinsic value

By Percy Venegas www.EconomyMonitor.com

Photo by Josh Calabrese on Unsplash

Photo by Josh Calabrese on Unsplash

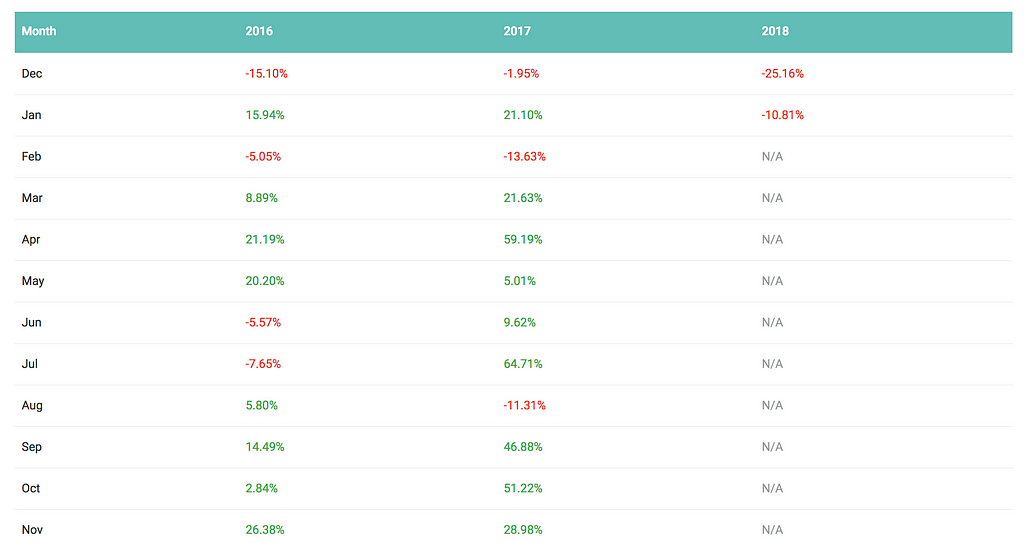

In their book “Beyond Smart Beta: Index Investment Strategies for Active Portfolio Management” Kula, Raab, and Stahn define Total return as the amount of value an investor earns from a security over a specific period when all distributions are reinvested. While it is still too early in the development of crypto assets to account for all distributions (dividends, coupons, capital gains), it is customary to use at the very least the price increase to measure the investment’s performance.

Typically, those historical returns would be the “goal” in a predictive model catered to “learn” (in an interactive fashion) what demand signals are also signs of value appreciation.

BTC and BCH historical monthly returns. Source: Coincheckup

BTC and BCH historical monthly returns. Source: Coincheckup

In our paper Crypto Economy Complexity, we argued that crypto economies tend to converge to the level of economic output that can be supported by the know-how that is embedded in their economy — and is manifested by attention flows. And, since a fork is really an event at the macroeconomic level (for instance, the economy of BitcoinCash vs the economy of Bitcoin), the aggregate demand for output is determined by the aggregate supply of output — there is a supply of attention before there was demand for attention.

We also discussed the practicalities of quantifying economic complexity by ranking economies, focusing on the specific case of cryptocurrencies and tokens. Here we will demonstrate how to develop the heuristics of such an approach. But as we will see, a more fundamental question about value arises:

Are the nodes running blockchain software essentially a material expression of people’s beliefs? Particularly, is the “belief consensus” the fundamental source of intrinsic value, than can be measured by intangible attention flows and tangible transaction activity?

Demand flows

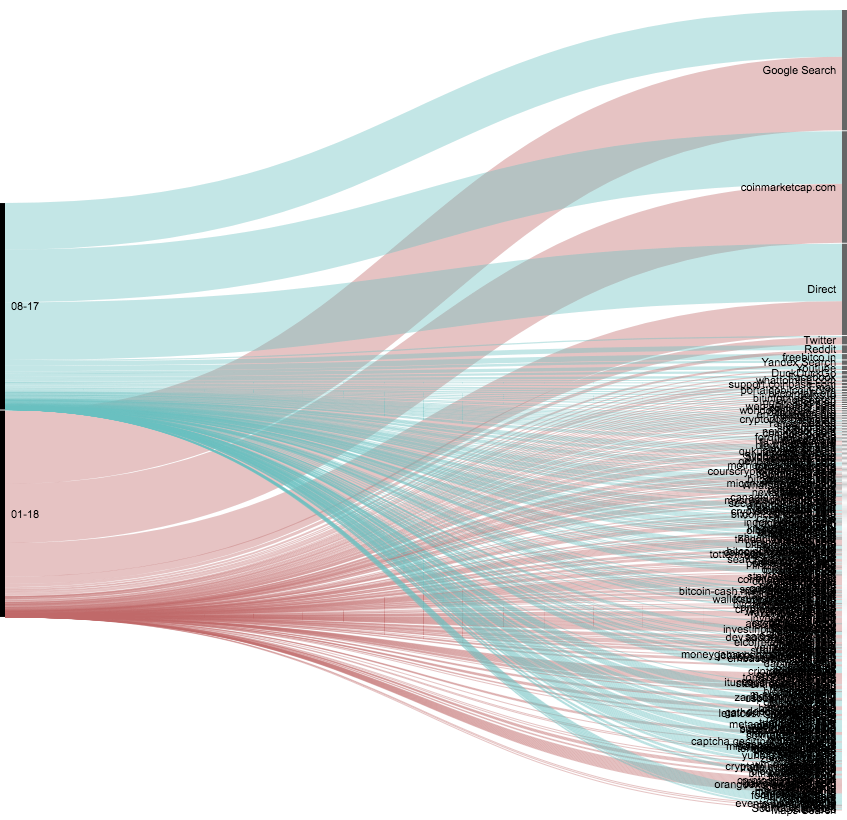

When a blockchain split event occurs, a race (competition) for attention begins. Demand stars flowing from search engines, price trackers, faucets, wallets, education sites, and the many services that support a crypto economy. What is notable here is that the flows include almost every service that one should expect on any economy, even if those are not directly related to cryptocurrency: entertainment (e.g. games), art, jobs, and so on — in other words, the idea that what is happening in crypto currency markets is only fueled by financial speculation is misleading.

The image shows the attention flows to a sample from the BitcoinCash economy, in the period of August 2018 and January 2018. Note how signals that are expected to build-up over time (e.g. search engine traffic) are naturally bigger when the economy is more mature, how there are dominant sources, and how a myriad of smaller sources make up for the rest of the flows (roughly 60% during both August and January).

Bitcoincash inflowsTraffic share

Bitcoincash inflowsTraffic share

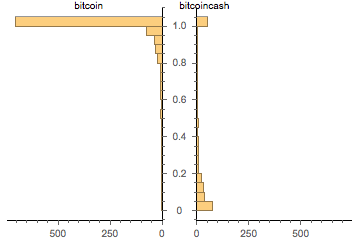

We sample the top 1000 sources that are shared by both Bitcoin and BitcoinCash over a period of 6 months, from August 2017 to January 2018. We see how the distributions are different: Bitcoin captures the larger share of traffic from most sources (80% or higher), while BitcoinCash has more sources that are small contributors (20% or lower).

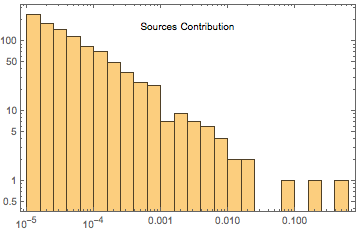

Paired histogramContribution

Paired histogramContribution

However, the “market share” of each attention economy has to be modulated by the contribution of each source — as we saw before, some sources have a disproportionately large weight. Here we look at the aggregate contribution from all sources towards both Bitcoin and BitcoinCash, across 6 months. We see how the dominance of 3 sources is clear, while there are hundreds of smaller contributors.

Log, LogCountsShare over time

Log, LogCountsShare over time

To better understand the shape of the data we construct an array, in which the vertical axis represents the passage of time (from August at the top, to January at the bottom), the cells in the horizontal from left to right are each one of the first 200 sources (we take this smaller sample from the top contributors from the 1000 sources, for simplicity of analysis and visualization), and the colors encode the traffic intensity (yellow is high, blue is low, red is no data).

Bitcoin

Bitcoin BitcoinCash

BitcoinCash

We see that Bitcoin has a virtual monopoly on attention (there is very little red on its chart). There is also no apparent overlap in the top sources for each crypto-economy — this is a sign of specialization. For instance, some forums clearly chose the Bitcoincash camp, and some statistics services adopted BCH as their niche specialty (or became favorites of the BitcoinCash community). Over there, BitcoinCash wins the contest for attention — but since the contribution of those sources to the overall Bitcoin-BitcoinCash economy is small, their positive impact on creation of value is not certain.

One thing that is striking to see is that time did not make things better for BitcoinCash: there is some creative destruction in the form of services that BitcoinCash came to dominate later, but there are not really many. And few more that did not exist at the beginning came online later as developers started building tools specifically for this economy. But in general, the ones that were strong at the beginning remained so across the whole period of time.

Ranking

The first thing that we should note is that these are fat arrays — that is, they have too many variables and very few observations. This is by itself a challenge for most machine learning techniques unless an evolutionary algorithm is used.

Predictive model

When we start learning ranking models, we interpret returns as an indication of value, and the demand signals from traffic sources as the drivers of that value. Since we are constructing a ranking system, we are interested in the demand relationships that optimize BTC_returns > BTC_returns.

The first formula that we discover what may appear as a trivial model: the returns of BCH are larger when the influential site Bitcoin.com, an advocate of BCH that also operates a wallet service, throws its weight to support BCH.

model 1

model 1

We keep running new generations of our evolutionary search, and more informative relationships emerge; non-mainstream search engines where demand signals begin to pop-up, also mining pools, and even informational sites. Several iterations can be run, and if we do it over larger sample sizes (instead of the 200 sources, we use the original 1000, or even 10.000) and more time periods (temporal steps measured in weekly or daily returns, instead of months), likely many other interesting relationships will appear.

model 2, first run

model 2, first run model 2, second run

model 2, second run

This diversity points to an interesting fact: we should perhaps trust model ensembles, rather than standalone models. And this makes sense: while in classical Economic Complexity theory (Cesar A. Hidalgo)one deals with relatively unchanged basket of products that are produced by the same countries, in a crypto economy new sources of attention are born and die constantly, and the sinks of that attention (the economies of each network) also are created at any time that a fork occurs and a community rallies behind the new coin. Our best anti-fragile ranking system is that one that is flexible and robust — as the crypto-economies that are being analyzed themselves.

Conclusion

Digital assets detractors usually say that there is no proven demand for cryptocurrencies, but we have demonstrated that demand not only can be measured, but that crypto-economies can be ranked as demand evolves. Perhaps the exercise of comparing Bitcoin and BitcoinCash is not entirely fair (after all BTC had the first mover advantage), but the heuristics that we have learned from the data have relevant applications nonetheless. For instance, one could identify what are sources of systemic importance, or what traffic is overpriced or underpriced. And since in blockchains transaction count and exchange volume can be faked by batching transactions and other tricks (not to mention rampant market manipulation, of what the BCH whales have been charged more than once), one of the viable measures of value might be actual supply and demand of attention.

Furthermore, if crypto assets defy the “Efficient Market Hypothesis” and the idea that all available information is encoded in prices, something more profound may be going on here: beyond any of the traditional definitions of utility, disintermediation of trust by itself might entail a premium.

In that case, the value of the chain may reside on the chain itself: the nodes running the software are simply an expression of people’s beliefs — being that the belief that the market can be manipulated for personal gain, that it is about time to challenge the government monopoly on money, that algorithmic money might be the more convenient utilitarian artifact to conduct transactions if you have already digitized a large part of your day-to-day activities, or else. This belief consensus is a human-machine construct, and perhaps this is why economists who are not trained as technologists have a hard time grasping the implications.

But what is more intriguing is that what the quantitative analysis reveals is not conflicting at all with the definition of intrinsic value — value is, after all, a matter of perception. So the argument that cryptocurrencies have no intrinsic value is without merit, and as we have demonstrated, not backed by data.

The intrinsic value is the actual value of a company or an asset based on an underlying perception of its true value including all aspects of the business, in terms of both tangible and intangible factors. This value may or may not be the same as the current market value.

Published by www.EconomyMonitor.com

Information provided for educational purposes only, should not be construed as financial or legal advice.

Recommended reads Crypto economy complexity

Publication date

Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not reflect the views of Bitcoin Insider. Every investment and trading move involves risk - this is especially true for cryptocurrencies given their volatility. We strongly advise our readers to conduct their own research when making a decision.