Latest news about Bitcoin and all cryptocurrencies. Your daily crypto news habit.

Bitcoin struggles with three main issues: high transaction fees, slow confirmation times and high volatility. In addition, I see a fourth issue: price appreciation, as the size and value of the network increases. The first two technological challenges could potentially be solved by innovations such as the Lightning Network and the third one could simply be due to the immaturity of the market. The fourth, however, is built into the fundamentals of cryptoeconomics and is unlikely to be solved. The cryptocurrency we will end up using as electronic cash in our day-to-day lives is likely to be some other than Bitcoin.

By now you are well aware of what Bitcoin is, where it came from, and are fully immersed in the cryptocurrency mania. When it comes to Bitcoin there are generally two types of people, either you:

- Have been in the game since late 2011 because you believe in the ideological concept of value accruing to the users of a network while disintermediating central third-party authorities

- Became an overnight expert in cryptocurrencies after you got in the game in July 2017, because your 17 year old cousin Billy told you how he just cashed out double your annual salary in 6 months

And if you don’t fall into either one of these and still don’t quite know what people are talking about, you can read this or this. Here we’ll dive into the shortcomings of Bitcoin instead.

Bitcoin’s status has gone from a revolutionary digital, decentralized peer-to-peer payments system to a digital store of value mimicking gold to a network of evangelists, explaining to each other how their respective holdings are valuable even when they hold little utility value. There are multiple posts out there on reason as to why this has happened — ranging from poor governance to inefficient scaling of the technology (yes, the two are linked), leading to high transaction fees and slow transaction times. So what’s going on?

Currency or money performs 3 main functions:

- Means of exchange: we can exchange currency for goods or services (or other currencies), as opposed to trading goods or services directly

- Unit of account: currency enables us to standardise the value of goods and services and compare them with each other

- Store of value: when we aren’t exchanging currency, it can act as a liquid value reserve

The original vision for Bitcoin was to serve as “a purely peer-to-peer version of electronic cash”, i.e. disrupting all 3 functions. This is only natural, as they are so tightly interlinked. In order to pay for a pizza in BTC, I need to know how much it costs in BTC and I need to be able to keep that amount in my wallet, in case I want to spend it tomorrow or next month.

Today, while some people are still adamant that Bitcoin will become the payments system of choice in the cryptocurrency realm, others have shifted the tone towards Bitcoin functioning solely as a store of value. This is largely due to 3 key reasons:

All three of these problems are real and any one of them already on its own would make it challenging to adopt Bitcoin as a widely accepted and used means of payment. 1. and 2. are technological scaling issues while 3. is a market immaturity issue. Many people are working on potential solutions for these, but before diving into those, I’d like to propose an additional issue:

4. Built-in price appreciation

This relates to the fundamental characteristic of cryptocurrencies with a capped supply, in which their value increases with the size of the network. This issue is not discussed to a similar extent as the first three.

Scaling issues

These days the Bitcoin scaling issues are talked about everywhere. The issue stems from the block size limit — only 1MB worth of transaction data can be confirmed per block — and the block creation time — it takes around 10mins to create a block. This means that a limited amount of transactions can be confirmed and as volume increases, users either have to wait longer for their transaction to be confirmed or pay more fees to miners to prioritize their transaction (or both).

Fees: The fee miners are charging skyrocketed at the end of 2017, reaching over $50 in December. Not buying a pizza with fees like that. They have, however, come back down to pre-December levels (largely due to a decrease in volume) but are still several dollars per transaction on average.

Time: Bitcoin averages 3 transactions per second (compared to Visa’s 2,000 tx/s) and the more transactions take place, the longer you have to wait for a confirmation. Some transactions have taken days!

Now, if you are making large one-off transactions, like buying a lambo or a Miami mansion, you are unlikely to care about a $100 fee and a few hours of confirmation time. However, these are significant issues when you want to pay for your 5-cups-a-day of coffee or the 7 individual articles you choose to read on a news site.

As these are technological issues, there are several people working hard to solve them, or at least to find workarounds. One of the most prominent solutions includes building a layer on top of the Bitcoin blockchain to handle certain activities, e.g. microtransactions. The talk of the town is Lightning Network (LN) — an amazing innovation in which off-chain payment channels enable multiple back-and-forth (almost) instant transactions for free. The LN transactions take place off-chain and are only validated on the Bitcoin blockchain once the channel is closed. Transaction fees are paid only when you open or close a channel. Buy all the Starbucks you want. (Read more about LN here: 1, 2, 3.)

While LN is potentially huge for Bitcoin (and other cryptocurrencies), it still is a workaround instead of addressing the underlying issue. Another cryptocurrency, better technologically suited for scalable quick and cheap transactions, could equally benefit from LN.

Bitcoin is the largest network, which is valuable and one argument is to leverage this value by only patching the underlying issue. However, as cryptocurrencies are still nascent, we shouldn’t limit ourselves to what is become a legacy technology. It’s a bit like deciding to upgrade steam engine trains to maglevs instead of designing airplanes just because we already have a vast rail network. Maglevs are cool but we should build airplanes as well.

Bottom line: potentially solved by off-chain solutions such as Lightning Network, but we could be better off adopting a currency that is scalable already on its own (with LN increasing its utility even further).

Price volatility

Bitcoin daily volatility over the past year ranged between 1.5% and 8.2%. For reference major currencies average between 0.5% and 1.0% while gold averages slightly over 1.0%.

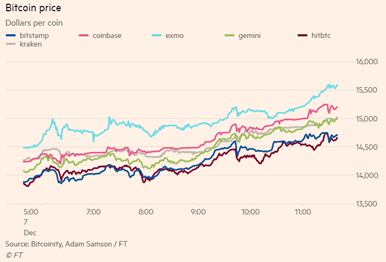

What I find curious is that people only ever talk about daily price volatility. While Bitcoin daily volatility already is high, we know that it tends to make giant leaps or drops over a few days or weeks, making the daily volatility a short-sighted and insufficient metric. If we look at the price changes over a longer period of time — e.g. 30 days — the average volatility over the past year was 58% while for the past three months it is 103% (due to the December rally and subsequent January plunge). For reference we can compare these figures with the 30-day price volatility of gold, which over the same period of time averaged 3.0% and 4.5%, respectively. Now you can see that the difference is alarmingly high. How can an asset which is 20x more volatile than gold be used to store value, compare prices, let alone transact? Simple: it can’t.

But there is an argument to be made that this is simply due to the immaturity of the asset class. Similar to how the adoption of any novel technology goes through turbulent phases of soul searching when finding the right use-case and best way position it to customers, Bitcoin too is still looking for its place in the world. There is still lots of ambiguity and uncertainty e.g. in terms of regulation, and constant changes in how governments and financial institutions treat the asset make it impossible to take a long term view, fuelling large fluctuations. On top of this the trading volumes are still relatively low, leading to an inefficient market. This is evident from the price gap across exchanges (which in an efficient market would quickly be arbitraged away).

Bottom line: Once regulators figure out how to treat Bitcoin, increased volume makes it a more efficient market, and the asset class matures more in general, the volatility problem should peter out. This issue could therefore iron itself out over time.

Price appreciation

Metcalfe’s law states that the value of a network is exponentially proportional to the size of the network — originally referencing the value of a telco network with n connected users being n^2. This simple idea applies to any network: roads, Facebook, the internet, or cryptocurrencies. However, what is novel about cryptocurrencies is that we are not only able to value the network but this value is distributed to the users of the network in a quantifiable, liquid form. Sure, the broader a road network is the more convenient it is for me (except in LA), or the more users Facebook has, the better I can connect with friends (in theory), but… that’s it. I can’t decide one day that I want to diversify my value holdings and shift my Facebook value to Twitter value. The quantifiable, liquid value accrues to Facebook Inc and its shareholders.

Cryptocurrencies are different. The network value of a cryptocurrency is quantified in its price and directly attributed to the user who owns the currency. Indeed, one analyst estimated that 94% of Bitcoin’s price fluctuation over the past 4 years was explained by the number of users and average transaction value. Thus, the more widely Bitcoin is adopted, the more upward price pressure there is. That value accrues to the user may seem obvious in the case of Bitcoin (obviously I get the value of the currency I hold), but if you consider other cryptocurrencies, this is more interesting. E.g. Steemit, a social media platform, which increases in value with the number of users and quality of content — directly attributed to the users of the social network.

In order for me to use a currency as a means of exchange or a unit of account it needs to be stable. Most fiat currencies are stabilized by a central bank controlling interest rates and money supply. Bitcoin does not have this luxury but rather a build-in price appreciation mechanism (or deflationary mechanism, depending on how we think about the asset). If I expect my Bitcoin to be more valuable tomorrow (i.e. if I expect a good or service to be cheaper tomorrow in BTC terms), I certainly won’t spend it today.

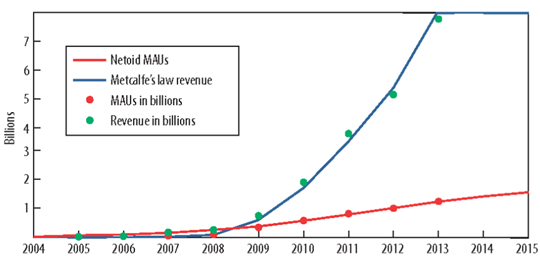

Some people might argue that Metcalfe’s law is an oversimplification and that the network value will eventually see diminishing returns, yielding a curve shaped more like an S-curve than an exponentially growing one. In 2013 Bob Metcalfe published a study assessing the growth of Facebook’s userbase (following a netoid S-curve) and its associated revenues (following Metcalfe’s law), and the results speak for themselves:

So far there is no indication that the price appreciation effect would diminish.

To solve this, teams are working on different approaches to create stablecoins (e.g. Basecoin, Maker, Tether, TrueCoin), with their value pegged to another asset in one way or another. The different ways in which these approach price stability is hugely interesting. (However, not everyone believes in this either.)

Bottom line: Bitcoin price appreciation due to increased network size is unlikely to be solved, meaning that users will not spend the asset. Stablecoins could potentially be a solution to this, but that is not much relief for Bitcoin.

So if Bitcoin will never be a widespread means of transaction, why is it so valuable? Precisely because of 4. The network value is distributed to the members of the network. As long as we think there is value in this network, Bitcoin will be priced accordingly. The value of the Bitcoin network might diminish if another cryptocurrency proves that it can fill the role of a means of exchange. It will need to have better scalability infrastructure, reach maturity to tackle volatility, and whether price appreciation is solved by a stablecoin or some other novel hybrid solution remains to be seen. But the bottom line is: Bitcoin will never be your purely peer-to-peer version of electronic cash.

Would you agree? Do you disagree? What do you think the future cryptocurrency means of exchange will be? Are there any key characteristics you see in cryptocurrencies already available today? Please let me know what thoughts this post evoked.

Bitcoin will never be your peer-to-peer version of electronic cash was originally published in Hacker Noon on Medium, where people are continuing the conversation by highlighting and responding to this story.

Publication date

Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not reflect the views of Bitcoin Insider. Every investment and trading move involves risk - this is especially true for cryptocurrencies given their volatility. We strongly advise our readers to conduct their own research when making a decision.