Latest news about Bitcoin and all cryptocurrencies. Your daily crypto news habit.

A visualization of the Bitcoin network (from Satoshi Nakamoto’s white paper)

A visualization of the Bitcoin network (from Satoshi Nakamoto’s white paper)

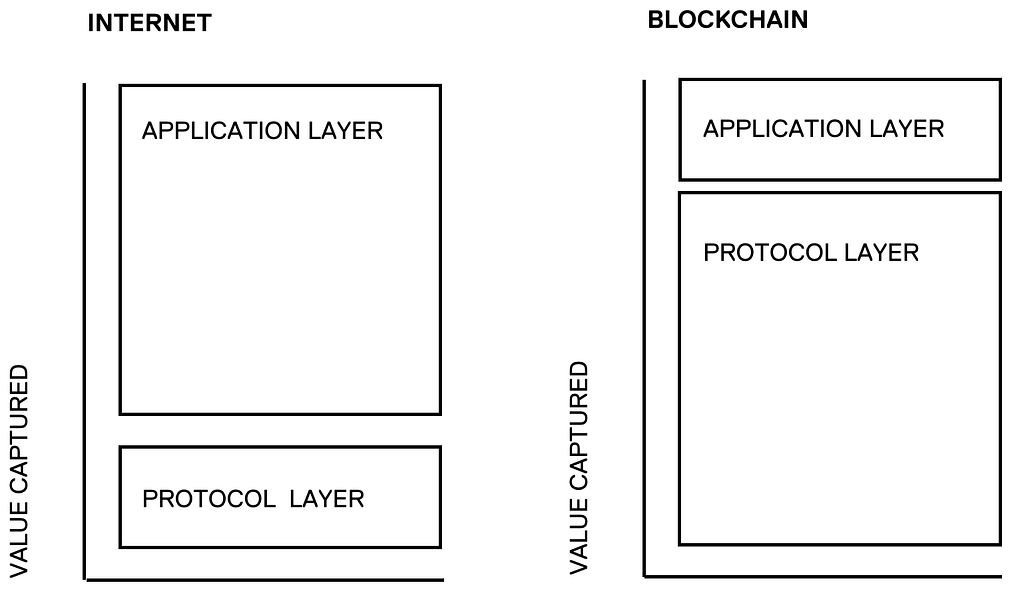

It is challenging to value crypto protocols. The “fat protocol” thesis represents an attempt to assess the value of crypto networks. The thesis — which has been put forward by Joel Monegro in 2016, who was at that time at Union Square Ventures — posits that the value of blockchains will concentrate at the protocol layer. Whereas in the case of the protocols underlying the Internet (such as TCP/IP, HTTP, or SMTP) value has been captured at the application level, the thesis states that the value of blockchains will be distributed along the protocol layer. Monegro argues that whereas the Internet is composed of “thin protocols” and “fat applications,” the inverse relationship holds in blockchains — blockchains will consist of “fat protocols” and “thin applications“ (see Figure 1).

The current distribution of value of the most dominant cryptocurrency and blockchain protocols seems to support the “fat protocol thesis” — more value appears to accrue at the protocol layers, such as Bitcoin and Ethereum, than to applications built on top of these protocols. Bitcoin’s market cap, for example, is currently at around 140 billion USD while the largest Bitcoin-based companies are valued at around one billion USD.

But how plausible is the “fat protocol” thesis? This article will challenge the fundamental assumption that most value of protocols will be extracted at the protocol level. It will argue that the value captured depends on the nature of the protocol. Before we develop the arguments against the “fat protocol” thesis, we will briefly have a closer look at different crypto protocols.

Crypto Protocols

The plethora of existing cryptocurrencies and protocols can broadly be categorized as utility and store of value protocols.* Whereas smart contract platforms, such as Ethereum or EOS, are utility protocols on which distributed applications (or Dapps) can be built, Bitcoin can be considered to be a store of value protocol. Now, to assess whether the value of utility or store of value protocols will indeed concentrate on the protocol level, we need to understand how these protocols create value. It is interesting to explore Ethereum a little bit further, which has currently a significant market cap.

Ethereum has multiple use cases, such as providing the infrastructure for processing smart contracts operations and building various Dapps, or DAOs (Decentralized Autonomous Organizations). If the “fat protocol” thesis holds, then value would be distributed along the Ethereum protocol layer as it supports the various applications that can be built on top of it. But will all the different potential use cases of the Ethereum protocol, and a high network transaction volumes, translate into a high price of Ether, the native cryptocurrency that enables the operation of the Ethereum network?

In order to ensure that the cost of using Ethereum as a smart contract platform is as low as possible, the Ethereum developers built the so-called GAS mechanism into Ethereum, which decouples the cost of using the network from the value of Ether, the platform-native cryptocurrency. GAS is required to perform computing operations or storage on the Ethereum network. As John Peffer has shown, the price of GAS will, in the long term, converge towards the marginal cost of computing. If the cost of running operations on the Ethereum network would be substantially higher, users would simply switch to another, less expensive, smart contracts platform, or fork it to create a cheaper version of the Ethereum blockchain with similar functionality. In other words, given the decoupling of GAS and ETH, the development of many use cases and high network transaction volumes do not necessarily fuel the value of the cryptocurrency that is imbedded into the protocol.

Now, it could be argued that ETH could have an arbitrarily high value due to speculation. However, as frictions to holding cryptocurrencies decrease and interoperability between utility protocols becomes possible, it seems likely that users do not need to hold an inventory of a specific utility token as they can always be acquired for a particular purpose when needed. Instead, it seems to make more sense to store value in the dominant pure store of value protocol.

It, thus, seems that most of the value in the case of Ethereum will accrue at the application layer as the network provides the execution of smart contract operations. For this service, end-users will pay a certain price. However, the cost of executing a smart-contract should be as low as possible — without becoming unprofitable for miners — and should not deviate at equilibrium from the cost of the computational resources consumed. Also, decreasing costs in computation and the fact that these networks are open source — which allows competitors to fork the networks and provide a similar service for a lower price — will likely put further downward pressure on marginal costs and prices. It is precisely the open source nature of crypto protocols, which allows the code to be forked, which represents a further challenge to the “fat protocol” thesis.

Forks and Interoperability

As already mentioned, blockchain protocols have the feature that they can be forked. A so-called “hard fork” occurs when an existing cryptocurrency’s code is changed so that the cryptocurrency splits into two versions. The most well-known fork is the Bitcoin hard fork of mid-2017, in which Bitcoin Cash forked from Bitcoin’s codebase. In other words, forks enable the creation of a myriad of competing protocols. However, while forks might enhance utility for users (as they can result in decreased costs or enhanced functionality), they can dilute the value of a protocol. So, if there is a concentration of value in a utility protocol — i.e., the protocol becomes “fatter” — it is likely that a fork will occur, which provides a similar or a specialized functionality at lower cost and/or increased efficiency. Thus, forking could make it difficult for value to concentrate at the level of an individual utility protocol. Concentrated value, or a high market capitalization of a utility protocol, provides incentives to fork the code and create a new network. While the protocol layer as a whole might become “fat,” it is more plausible that most individual utility protocols remain relatively “thin.”

Will Crypto Protocols Be Fat or Thin?

As Pfeffer has argued, the open-source and forkable nature of utility protocols will likely tend toward a fragmentation of use cases and protocol functionality — applications built on top of a specific utility protocol will likely be protocol agnostic and users capable of switching between different protocols. In contrast, a store of value protocol, such as Bitcoin, will be able to capture a less fragmented market and far more value than a utility protocol (when compared, for example, to the total value of gold bullion and foreign reserves). Ultimately, however, the “thinness” and “fatness” will most likely depend on the function a crypto protocol performs.

Moreover, in addition to the forkable nature of crypto protocols, interchain interoperability seems to further minimize the potential value capture of utility protocols. Developments such as so-called atomic swaps — which are smart contracts that enable the disintermediated exchange of cryptocurrencies — will substantially lower the costs of switching between blockchains. The frictionless interoperability between different crypto networks will most likely drive down the value of utility tokens further as users will — in contrast to a store of value cryptoasset — not need to hold any inventory of a utility cryptoasset. In this case, liquidity would naturally gravitate toward a single store of value protocol for convertibility.

Given the above-mentioned dynamics of crypto protocols, it, thus, seems that the value capture of utility protocols is limited by their forkable and interoperable nature. In the case of utility protocols, it appears that most value will be extracted from the application layer as developers can provide specialized and proprietary applications, such as specific smart contracts. It could even be the case that utility protocols will not retain any value whatsoever, as utility models can be made compatible with bitcoin, which, in turn, could be more efficient.

On the contrary, a store of value protocol, such as bitcoin, will likely be far more valuable as its has strong networks effects and is able to capture a larger and non-fragmented market. Whereas bitcoin will most probably dominate as a store of value protocol, the value of utility protocols will be fragmented across different and specialized use cases. In other words, while a store of value protocol will most likely become “fatter,” utility protocols will most probably become “thinner.”

*Ultimately, “store of value” and “utility” properties are interrelated. Bitcoin could be described as a utility protocol as well — Bitcoin’s utility is transacting value. Conversely, in the case of utility protocols, despite claiming to be “utility”-focused, these utility protocols have tried to strap a store of value token to their network. Their utility relies on the tokens having value. The distinction between store of value and utility protocols should help explain the different use cases and functionalities of crypto protocols.

Thanks to Murad Mahmudov and Neil Woodfine.

What Makes Crypto Protocols Valuable? was originally published in Hacker Noon on Medium, where people are continuing the conversation by highlighting and responding to this story.

Publication date

Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not reflect the views of Bitcoin Insider. Every investment and trading move involves risk - this is especially true for cryptocurrencies given their volatility. We strongly advise our readers to conduct their own research when making a decision.