Latest news about Bitcoin and all cryptocurrencies. Your daily crypto news habit.

A Radical New Way of Valuing Methods of Payment

One still little-understood aspect of Blockchain smart contracts is their ability to create what is nothing short of the first real form of currency investment in the world.

By using the term investment here, I am being specific. A currency is something used to pay for something with. It is not conventionally an investment at all, nor a reliable one at that (even in cryptocurrencies this is mostly true). Buying USD and then applying 1,000x leverage against CHF is not investing, it is speculating. Investing means buying something so that it gives the holder a return on investment (ROI), which is manifest in the form of an income receipt.

When you buy a house, and someone pays you rent, that’s an investment return, separate from a speculative return, which indicates how much the asset went up in fiat value during the holding period.

When undertaking an investment valuation, by far the most common approach is to use a discounted cashflow analysis to arrive at a net present value of the asset being valued. The formula for calculating DCF for an asset value in present terms that is three years into the future from now is expressed as follows:

PV = CF1 / (1+k) + CF2 / (1+k)2 + CF3 / (1+k)3 + [TCF / (k — g)]/(1+k)n-1

PV = CF1 / (1+k) + CF2 / (1+k)2 + CF3 / (1+k)3 + [TCF / (k — g)]/(1+k)n-1

where PV = present value, CFi = cash flow in year I, k = discount rate, TCF = the terminal year cash flow, g = growth rate assumption in perpetuity beyond terminal year and n = the number of periods in the valuation model including the terminal year.

There is no currency that has been valued this way as there is not an expected income receipt from a medium of exchange, clearly, since its utility is purely that of a payment utility.

With smart contracts, however, it is possible to create what is in effect a synthetic income receipt that is expected at some point in the future. This income receipt while not specifically a classifiable dividend or such is nevertheless manifest in the form of an income-style gain. This could end up having radical effects on the wider investment world as people catch on. Companies for example, can easily create their own currencies and pretty much self-fund their way out of debt with such an approach.

Futereum Smart Contracts — A Prototype

Around a year or so ago, I was involved in the creation of the first of these fascinating financial technologies. With Futereum Smart Contracts we started by using Fibonacci as an expression of the amount of Futereum tokens that one ETH receives in the process when it is sent to the Futereum token’s smart contract. We programmed the code so that number varies over time, and at the end of a fixed period, the smart contracts permit the holder of the tokens to swap back for an equally-distributed share of the contract’s supply of ETH. If you purchase an unequal share of something and then re-exchange it back on an equalised basis, you either stand to make or lose a lot of your original purchase sum back, and that is indeed the case here.

To fortify the product so that the chance of an investor losing was dramatically slimmed down, we next turned our attention to more experimental methods of shaking up swaps algos in smart contracts with the creation of Futereum Bitcoin and Futereum Markets. To make Futereum Bitcoin, we packaged over 4 additional separate smart contracts with 2,800 tiers of price and blocksize data (used for the quantity sold per tier) into a master contract which interacts with the main Futereum Bitcoin contract to achieve the result of effectively allowing the Futereum tokens (with ETH stored inside them) to become further re-distributed in a contract that mimicked in pricing the fluctuation of Bitcoin over its first 10 years of trading.

Next we used this strange “synthetic Bitcoin token” as the foundational token to make purchases of another proxy smart contract token that we called Futereum Markets. Futereum Markets is exchangeable for Futereum Bitcoin at a ratio that parallels the value of CoinMarketCap.com’s index divided by 1 billion. This allows a holder of Futereum Bitcoin to effectively speculate on the real-time price movements of CMC, the same way that predictive algorithms allow you to do, and the greater the increase in price of CMC, th dramatically better the odds of achieving a gain in ETH there is for the investor. To achieve this we built a separate external Oracle and configured the Futereum Markets smart contract to extract the relevant API data at 15-minute intervals 24/7/365 which is broadcast from and obtained by the Oracle off a standard CMC Pro feed.

The resulting scenario is one that looks like this when you factor all sorts of other fees, taxes and incentives we included in the contract code (which is not necessary to understand for the purpose of this post):

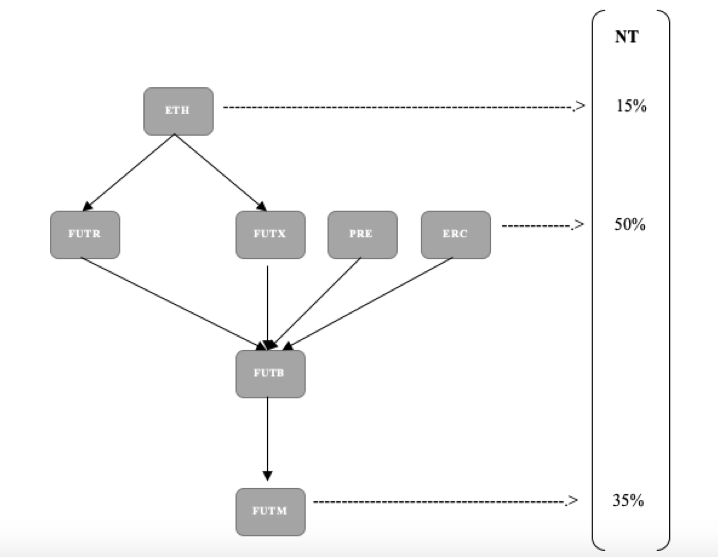

i. Futereum Bitcoin is a proxy purchased with Futereum, itself purchased with ETH.

ii. Therefore, Futereum Bitcoin is a “proxy of a proxy” for ETH. The result is one where at the end of 21 million units of Futereum Bitcoin issuance, all Futereum Bitcoin is equally exchangeable for a like-for-like percentage sum of Futereum (and other tokens on the network) that are stored in the smart contract until that point.

iii. Because Futereum tokens store ETH in its own smart contract, and yet much of the ETH that is stored therein is likely to become non-swappable for a long period of time as a result of the time that Futereum tokens spend sitting inside the Futereum Bitcoin smart contract the amount of ETH per Futereum token sent back to the smart contract is a lot as there is continuous build-up.

For the first time in history, an income calculation was able to be applied using DCF methods only reserved for conventional income assets on what was this time a currency. The impact of that cannot be understated. Suddenly, we don’t require all the financial infrastructure to manage an economy as we did before! Interest rates no longer govern value!

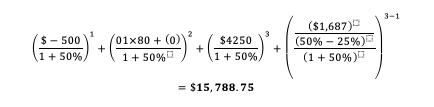

Using the equation above, which is how all VC’s value start-up companies, if we want to calculate a very simple net present value for one ether invested Futereum at the point that the Futereum token is invested in Futereum Bitcoin the calculation on a discounted cash-flow basis is:

As displayed here clearly, the value of 1 ETH (at $500 for example’s sake) has a net present value automatically, merely by positioning it inside the smart contract algorithm of over $15,000. The result is a net present value gain of 29,000%, and this is discounting at an aggregate compound rate of 50% a year, an incredibly unlikely event in and of itself.

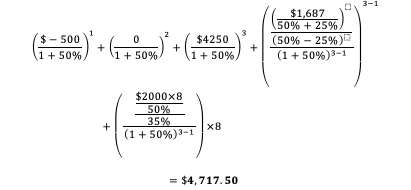

Let’s take this up a level now. When we purchase 114 Futereum tokens for 1 ETH while the Futereum smart contract is selling in the first of ten tiers, by the time the exchange of all Futereum and all Ether takes place, assuming that the total number of tokens that count be issued are so in year two, then we would be able to value the FUTR’s net present value discounting the asset at a comparable rate of return we might achieve in the underlying asset.

Assume that ETH is $500, and that you expect to receive 8x the amount of Ether from the Futereum smart contract as per the realistic probability of doing so if all the tiers of the smart contract are sold out somewhere in year two. Further, you assume that ETH has risen to $2,000 by three years’ time and that the growth rate going forward is 35% (around half). The Futereum smart contract will not accept any re-exchange until year 3 if that is the case. Further, you estimate that you make around 50% profit per year trading comparable cryptocurrencies. Therefore:

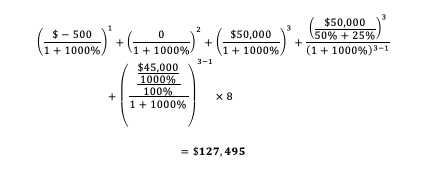

The result is that the value an investor obtains from the Futereum smart contract’s functionality is $4717.50 per Ether, representing what is a time-adjusted equivalent present value of an additional $4,267.50 when Ether is in the form of a Futereum digital note. Presciently, the DCF formula can be used to certify whether holding the actual underlying asset or whether purchasing whatever digital note proxy coin equivalent is a better bet. For instance, assuming that the appreciation of Ether is expected to be around 1000% per year for the next 3 years then:

In this case, our expected value for Ether in 3 years’ time is $50,000, with an additional $5,000 a year in future growth since we discounted the growth down by 10x after the realization of the investment and since Ether was growing at a rate of an additional 1000% per year during the invested period.

The critical point here is that the value at which we invest our $500 is enhanced with thousands in additional paper profits on a pure accounting basis just by storing the Ether is inside the Futereum smart contract. Clearly then, the ability to calculate currency values on the same basis that we do income-generating assets is a unique and unchartered innovation prospect.

The flexibility of smart contracts to make permissible discounted cash-flow valuations of cryptocurrency utility is perhaps the most exciting aspect of the smart contract build in terms of wider application to the investment world.

By allowing such valuations to be performed, currencies can quickly and easily be compared on a like-for-like basis directly with all sorts of investments, such as real estate, stocks, bonds and others. Further, such investments now that they have a discounted future value based on a specific income ratio equivalent, can be ascribed multiples for trading, in the way that securities are valued via the business cash flows.

Remarkably, all this is made possible without securitising a single portion of the digital currency unit as well, inviting the possibility for significant levels of disruption in equity and securities markets henceforth over the next few years.

Note: The Futereum project is open source and can be found at www.futereum.com

Smart Currency Income Instruments was originally published in Hacker Noon on Medium, where people are continuing the conversation by highlighting and responding to this story.

Publication date

Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not reflect the views of Bitcoin Insider. Every investment and trading move involves risk - this is especially true for cryptocurrencies given their volatility. We strongly advise our readers to conduct their own research when making a decision.