Latest news about Bitcoin and all cryptocurrencies. Your daily crypto news habit.

Buying your own home is usually a large financial commitment. It may be rather tough to qualify for a traditional mortgage from a brick-and-mortar banking institution. The common reasons for the denial are having a poor credit rating or not having a sufficient sum for a down payment.

If you find it challenging to qualify for regular home loan financing options or government programs, keep reading to find alternative ways to become a proud homeowner in Canada.

Why You Can Be Denied a Traditional Mortgage

Have you been rejected by a conventional bank? Thousands of Canadians have experienced this denial in Surrey BC, and are searching for alternative ways of getting payday loans. Big banks tend to decline applications from low-credit borrowers.

If your credit score is less-than-perfect, you may be rejected. So, it’s essential to keep your rating above average, but not every consumer can repair their credit immediately.

Furthermore, those who haven’t saved enough for a down payment can also be declined. Can you set aside 20 percent for a down payment? Your application will most likely be declined if your sum isn’t sufficient to qualify for a mortgage.

The Bank of Canada put some pressure on home loans and boosted rates to 4.25 percent. This is the highest level of interest since 2008. Inflation rates keep on being high, so this was the seventh rate hike during the past nine months.

The rate of inflation remained at 6.9 percent in October 2022. Hence, borrowers who aren’t eligible for a home loan from a traditional financial institution are often turned away.

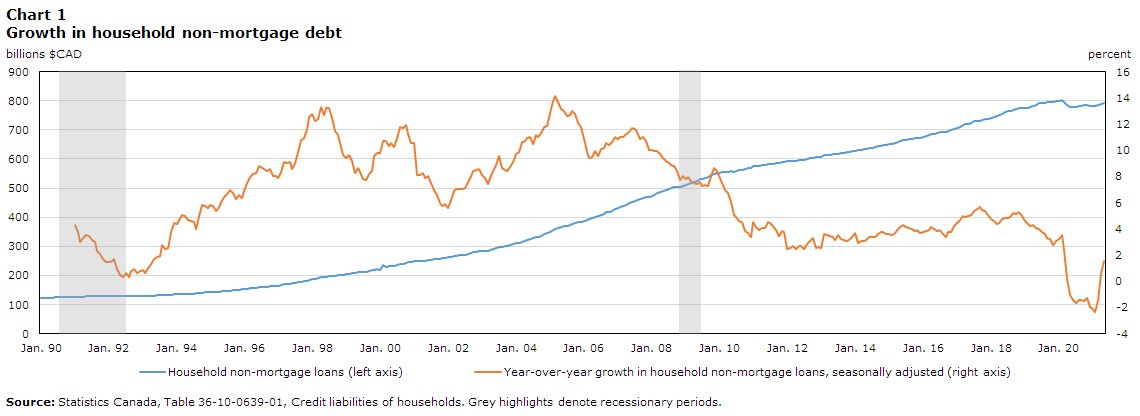

Statistics show that household non-mortgage debt in Canada has increased steadily since the mid-1990s, while interest rates kept on lowering in the early 1990s. More crediting options started to fill the market, and consumers had a chance to choose among these options.

Source: https://www150.statcan.gc.ca/n1/pub/11-621-m/11-621-m2021004-eng.htm

Year-over-year growth in non-mortgage debt slowed down during the global pandemic but began to grow again at the end of 2020. More and more Canadians take out household non-mortgage debt these days.

What Are the Alternatives?

If you are turned away from conventional banks, you still have options to fund this big-picture purchase and buy a home in Canada. Some consumers turn to private creditors. A-lenders are large banks in Canada.

Trust companies and credit unions are referred to as B-lenders. Those whose requests were turned down by brick-and-mortar banks may seek financial assistance at B-lenders. These crediting organizations are smaller but have also been around for several decades. They offer lower criteria offering more Canadians a chance to qualify for mortgages.

Those with inconsistent employment or credit who want more flexibility opt for these solutions. Of course, each alternative also comes with pros and cons. The drawback of alternative lenders is the demand to provide at least a 20% down payment.

Besides, you may encounter higher interest rates compared to conventional banks. Other businesses and family members might also serve as private lenders and offer more flexibility, but the rates will be much higher.

Alternative Ways to Get a Home Loan

Those who can’t meet the requirements and eligibility criteria to get a regular mortgage may turn to alternative ways of purchasing a home.

1. Get a Private Mortgage

Consumers with less-than-stellar credit may take out an unconventional mortgage from a private lender. Such creditors aren’t affiliated with a traditional bank. Such creditors can be other lending organizations or individuals. They offer fewer risks to the borrowers but charge a higher rate.

Peer-to-peer lending is one of the most suitable options here. You may want to borrow from your friend or relative, provided that you find a person who is eager to lend you the desired sum. The advantage of this option is having more flexible payoff conditions, while the downside is having to deal with potentially higher rates.

2. Pay Cash

This is another suitable alternative. Not every consumer will find this way realistic, but you should give it a try. More and more Canadians find it tough to save for a down payment as inflation rates keep on going up, and so do the cost of living and unemployment rates.

If you purchase in an affordable area, have saved a sufficient amount of cash, or have inherited a decent sum, this option may help you buy your own home.

The benefits are obvious – you don’t have to pay mortgage interest, remain financially independent, and save on property evaluation fees and closing costs. The drawback is that if you use all your funds to invest in a home purchase, you may have nothing left for your own needs. You may need to take out credit if you suddenly face monetary difficulties.

3. Rent to Own

What does this option mean? It means you make an arrangement with a seller to rent their for-sale home before purchasing it. The price for this property is predefined, so it may become a decent alternative for consumers who can’t set aside enough funds for a down payment.

Apart from that, borrowers with poor ratings may also choose this alternative. A fee for the right to purchase the property at the end of the lease may be asked to pay. Some owners don’t demand this fee, so you should negotiate the terms with the property owner.

A rent-to-own arrangement may be established with a long-term tenant who aims to buy the rental property. If the owner has issues selling their property, they can list it as a rental with a rent-to-own option.

4. Utilize Owner Financing

Some sellers may accept direct installment payments to sell their property. This alternative financing option is called owner financing. In other words, the seller funds your purchase while you make monthly installment payments to the property owner rather than a lending institution.

Until you pay the whole sum to the seller, the property title will be kept under the seller’s name. It can be tricky to find a seller who will be eager to use this option. On the other hand, this solution may eliminate certain banking expenses and be beneficial for both a seller and a buyer.

The Bottom Line

In summary, Canadians whose credit rating isn’t excellent and don’t have the necessary sum for a down payment may opt for alternative funding options. There are some ways to finance your home purchase and become a homeowner in Canada.

Publication date

Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not reflect the views of Bitcoin Insider. Every investment and trading move involves risk - this is especially true for cryptocurrencies given their volatility. We strongly advise our readers to conduct their own research when making a decision.